USA

USA

Canada

Canada

Australia

Australia

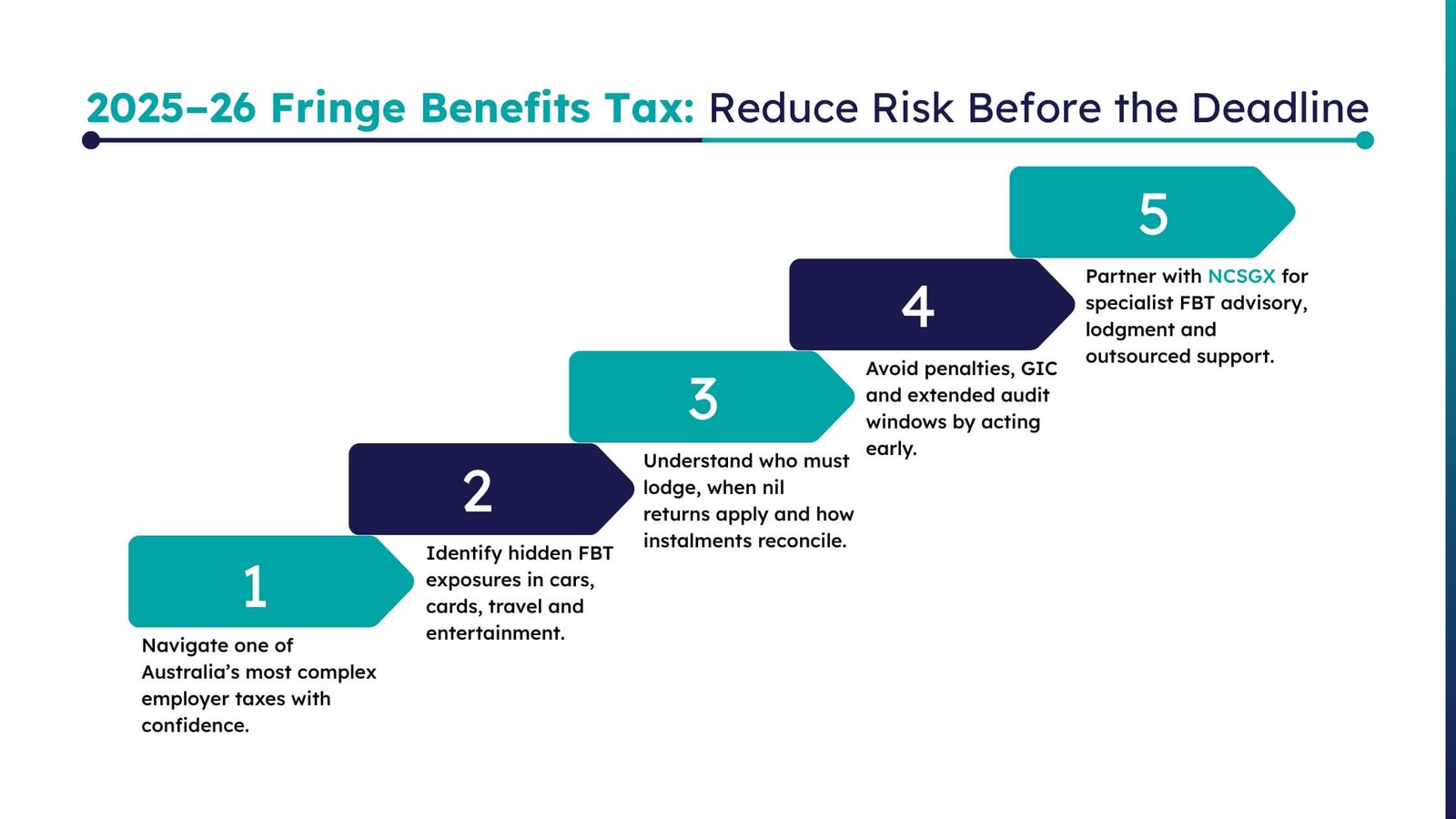

As the Australian taxation landscape evolves, the complexity of FBT remains a perennial challenge for all modern employers. For the 2025–26 year, NCSGX is monitoring ATO focus areas to ensure our clients maintain robust compliance and governance. The FBT cycle operates on a unique timeline that requires meticulous data collection and extremely proactive risk management. With the 2026 return deadline approaching, organisations must move beyond data entry to secure their tax-effective positions.

Clear visibility of your obligations ensures your business remains audit-ready during this era of increased regulatory transparency. Whether you provide company cars or salary-packaged benefits, knowing the exact deadline is critical for a seamless transition. Proactive preparation is not just about avoiding penalties; it is about protecting your firm’s reputation and financial health. Ultimately, a structured approach to the FBT year-end allows you to manage non-cash remuneration with complete confidence.

Understanding the 2025–26 fringe benefits tax year

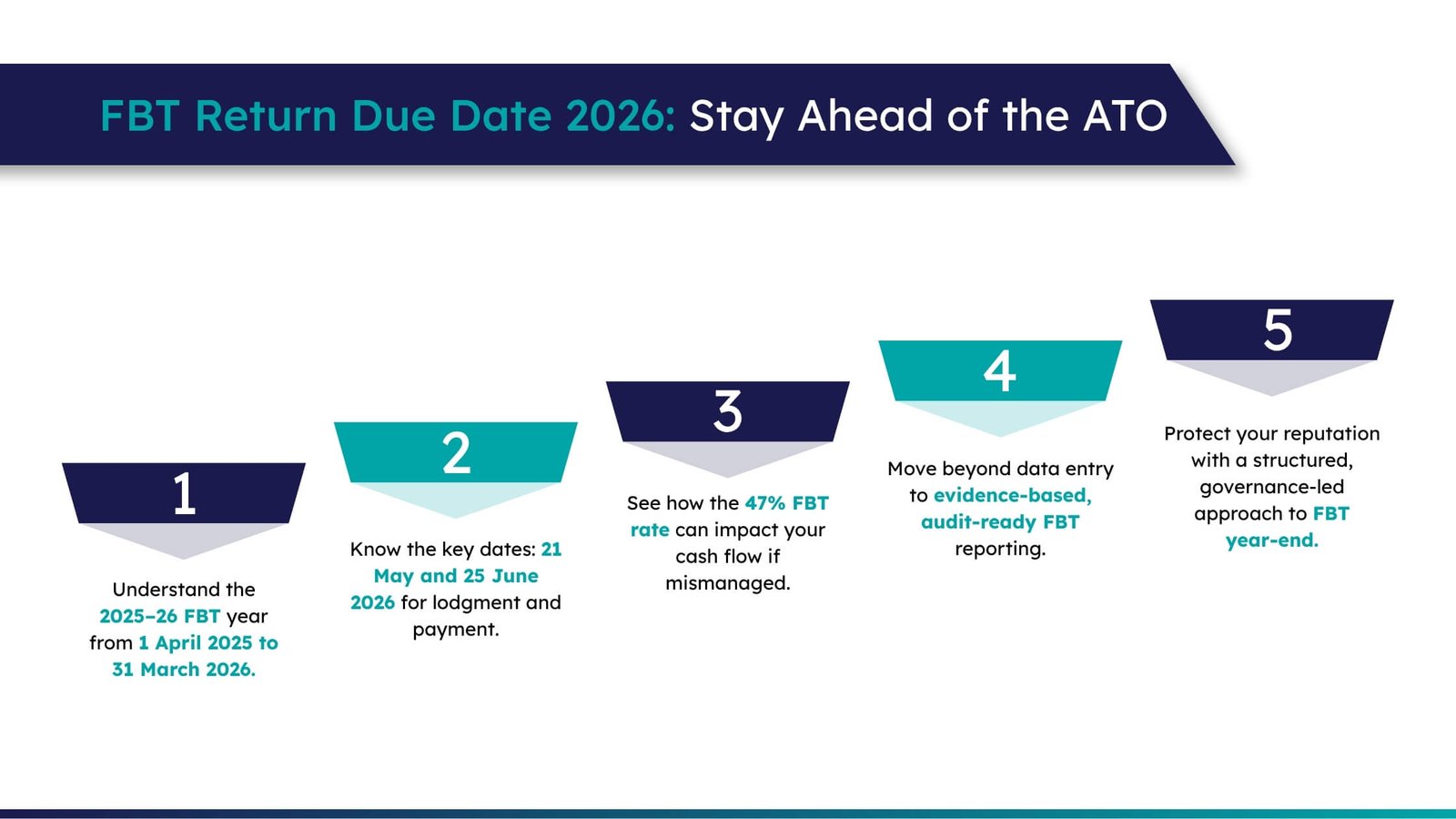

To navigate the 2026 reporting season, it is essential to clarify the specific timeframe at play. In Australia, the FBT year runs from 1 April to 31 March, which is distinct from the 1 July to 30 June income tax year. Consequently, the 2025–26 FBT year covers fringe benefits provided between 1 April 2025 and 31 March 2026.

- Fringe benefits tax is a tax paid by employers on certain benefits provided to employees or their associates in respect of their employment.

- These benefits are provided in addition to, or in place of, salary or wages, forming a critical part of an employee’s total remuneration package.

- In our experience at NCSGX, the high FBT rate of 47%, which aligns with the top marginal income tax rate plus the Medicare levy, makes it one of the most expensive taxes for businesses to mismanage.

- Many organisations still look to the fbt return due date 2025 as their reference point for timing, and while dates vary slightly each year, the core structure remains consistent.

- For the 2026 season, the ATO expects a high degree of accuracy in your fringe benefits tax return, requiring rigorous data substantiation.

- Attention is being directed toward benefits that may have been “hidden” in corporate credit card statements, staff travel expense claims, or meal entertainment accounts.

FBT return due date 2026: Key lodgment deadlines

The fbt return due date 2026 is determined by your method of lodgment. The ATO provides different timelines for those who manage their own tax affairs versus those who utilize a registered tax agent.

Standard Self-Lodgment Deadline

If you lodge your own return (for example, via paper or through the ATO Business Portal without an external agent), the standard deadline for both lodgment and payment is 21 May 2026. This is a hard deadline and missing it can trigger “failure to lodge on time” (FTL) penalties.

Tax Agent Lodgment Extension

Employers who lodge their 2026 fringe benefits tax return electronically through a registered tax agent generally receive an extension. In this case, the deadline is 25 June 2026. To qualify for this later date, your organisation must be on your tax agent’s FBT client list by 21 May. This extension is a valuable window for businesses with complex multi-entity structures or those managing diverse benefit types.

Key 2026 FBT Calendar Dates:

- 31 March 2026: End of the 2025–26 FBT year. All benefit data collection should be finalised.

- 21 May 2026: Standard FBT lodgment and payment deadline for self-lodgers.

- 25 June 2026: Extended lodgment and payment date for eligible electronic tax agent lodgments.

For detailed guidance on how to complete and lodge the annual return, the ATO provides the Fringe benefits tax return 2026 form and instructions.

Comparing these to the fbt return due date 2025 pattern confirms that the ATO maintains a consistent rhythmic expectation, allowing well-prepared finance teams to plan their workflows months in advance.

FBT payment due date and how payment works

The fbt payment due date is typically the same as your lodgment due date—either 21 May or 25 June 2026. However, the way you pay can vary based on your history of liability.

Quarterly FBT Instalments

If your FBT liability for the previous year was AUD 3,000 or more, you are generally required to pay quarterly FBT installments via your Business Activity Statements (BAS). These installments act as a “pre-payment” of your estimated 2026 liability.

When you lodge your annual return, you reconcile these instalments against your actual calculated FBT. This results in either:

- A “top-up” payment if your actual liability is higher than the installments.

- A refund if your installments exceed your actual liability.

The ATO’s automated systems are highly efficient at identifying late payments. Any amount outstanding after the fbt payment due date will likely attract the General Interest Charge (GIC), which is currently at a rate that can significantly erode your bottom line. At NCSGX, we advise clients to conduct a “shadow” FBT calculation in February to ensure their June cash flow accounts for any necessary top-up payments, often in collaboration with our outsourced payroll and fringe benefits tax support team.

Who must lodge a fringe benefits tax return?

A common compliance error is the belief that if there is no tax payable, no return is required. While this is true in some specific circumstances, you generally must lodge a fringe benefits tax return if:

- You have FBT payable on fringe benefits you provide to employees.

- You have paid FBT installments during the year (even if the final calculation is nil).

If you are registered for FBT but find you have no liability for the year and pay no instalments, you should submit a formal “Notice of Non-Lodgment” to the ATO. This prevents the regulator from following up on what they perceive as a “missing” return. The ATO explains these obligations in more detail in its guidance on lodging your FBT return and paying.

In practice, many employers overlook the need to lodge for benefits that are “otherwise deductible” or reduced to nil via employee contributions. However, without a lodged return, the statutory period for the ATO to audit those benefits remains open indefinitely. Lodging a return, even a nil return where appropriate, starts the “clock” on the amendment period, providing your business with greater long-term certainty.

Consequences of missing the FBT lodgment deadline

Missing the Fringe benefits tax deadline carries both financial and reputational risks. From a senior tax perspective, late lodgment is often viewed by the ATO as a sign of poor internal controls, which can lead to a higher risk rating for your organisation.

Potential consequences include:

- Administrative Penalties: These vary based on the size of the entity but can be substantial for mid-market and large corporations.

- General Interest Charge (GIC): Compounding daily on any unpaid amounts.

- Loss of Concessions: In some cases, eligibility for certain FBT concessions or exemptions may be contingent on the timely and accurate reporting of benefits.

- Increased Scrutiny: Once a business misses a lodgment, they are more likely to be flagged for “justified trust” reviews or data-matching audits in future years.

Working with a tax agent ensures that you manage these timelines effectively and provides a professional buffer in communications with the ATO.

Practical checklist to prepare for the 2026 FBT return due date

To ensure your organisation is ready for the fbt lodgement due date 2026, use the following checklist as a roadmap:

- Identify all Benefits: Review all General Ledger accounts for entertainment, travel, and motor vehicle expenses from 1 April 2025 to 31 March 2026.

- Finalise Logbooks: Ensure that all required motor vehicle logbooks are valid and reflect a representative 12-week period.

- Collect Closing Odometers: Capture odometer readings for all business-provided vehicles exactly as of 31 March 2026.

- Verify Employee Contributions: Ensure that any post-tax contributions made by employees have been correctly processed and recorded in the accounts.

- Reconcile BAS Instalments: Confirm the total amount of FBT instalments already paid through your 2025–26 Activity Statements.

- Confirm Lodgment Method: Decide if you will self-lodge by 21 May or engage a specialist to access the 25 June extension.

- Review ATO Focus Areas: Check your compliance against current ATO FBT rates and thresholds to ensure you are using the correct percentages and formulas.

By following this checklist, you can move toward the fbt return due date 2026 with the confidence that your data is defensible and your calculations are robust.

Conclusion: Securing your FBT compliance with NCSGX

Navigating the intricacies of fringe benefits tax requires more than just filling out a form; it requires a strategic understanding of how benefits impact your overall tax position and employer brand. The 2025–26 year is set to be one of increased oversight, and staying ahead of the Fringe benefits tax deadline is essential for any well-governed Australian business.

At NCSGX, we specialise in providing the technical depth and professional oversight necessary to manage complex FBT obligations. Our team can help you identify planning opportunities, manage your FBT advisory and compliance services, and ensure that your outsourced payroll and fringe benefits tax support is fully aligned with current legislation. By proactively engaging with the reporting process now, you can mitigate the risk of ATO intervention and ensure your final fringe benefits tax return is both accurate and optimized.

How NCSGX Can Help?

Navigating FBT obligations requires more than meeting deadlines — it demands strategic oversight, accurate data, and a defensible position if the ATO comes knocking. At NCSGX, we work with Australian employers to manage the full FBT compliance cycle, from benefit identification and logbook reviews to return lodgment and ATO correspondence. Our team ensures your organisation stays ahead of key dates, avoids costly penalties, and captures every available concession. To take the complexity out of your 2026 FBT return, speak with NCSGX today.