USA

USA

Canada

Canada

Australia

Australia

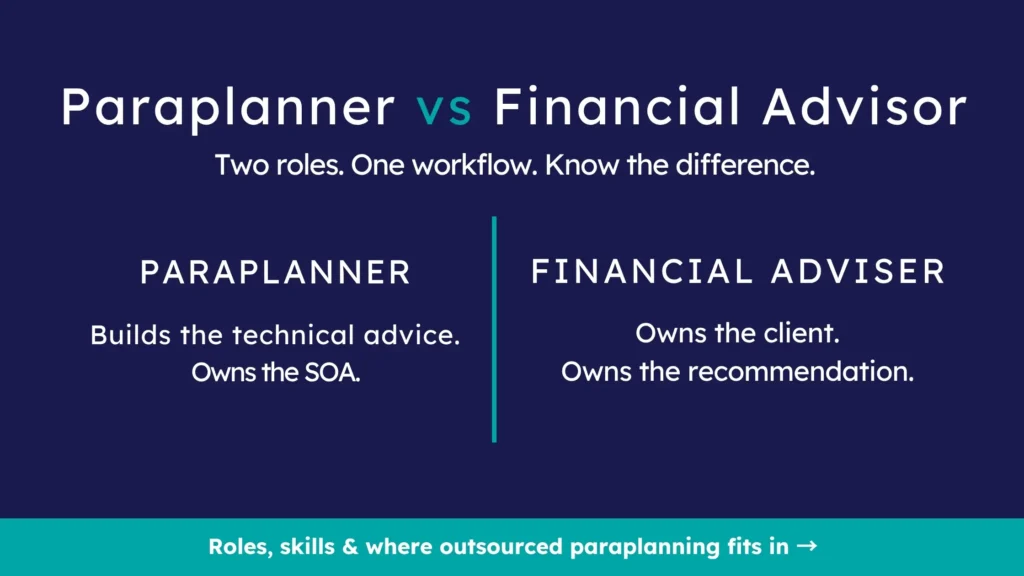

The Paraplanner vs Financial Advisor question gets asked most often by two groups: advisers thinking about hiring a paraplanner for the first time, and paraplanners weighing whether to sit the adviser exam. Both want the same thing: a clean line between the two roles, in one place.

Sitting across hundreds of advice files a year, the team at NCSGX puts that line in one sentence, the adviser owns the client and the recommendation, the paraplanner owns the technical build and the compliant documentation. The rest of this article unpacks what that looks like in skills, workflow, and capacity.

What Is a Paraplanner?

A paraplanner is the technical engine behind a financial advice practice. They take the adviser’s strategy and convert it into a defensible Statement of Advice (SOA) or Record of Advice (ROA). They run the modelling, complete product and platform research, prepare implementation paperwork, and make sure the file would stand up to an ASIC review or AFCA complaint.

For a deeper breakdown of the day-to-day, what does a paraplanner actually do in financial planning.

Typical paraplanner responsibilities:

- Drafting SOAs and ROAs against the licensee’s template

- Strategy: modelling TTR, contribution strategies, retirement projections, and debt restructuring

- Investment, super, and insurance product research

- File-note preparation and audit-ready documentation

- Compliance review against Best Interests Duty (BID), the Code of Ethics, and licensee policy

A paraplanner doesn’t sit in front of the client. They sit beside the adviser, translating the strategy conversation into a document that satisfies the Corporations Act s946A and the licensee’s audit framework.

What Is a Financial Advisor?

A financial adviser is the licensed professional who scopes the client’s goals, recommends a strategy, presents the advice, and owns the ongoing relationship.

In Australia, an adviser must:

- Be listed on ASIC’s Financial Advisers Register

- Operate under an Australian Financial Services Licence (AFSL), either as the licensee or as an Authorised Representative (AR)

- Hold an approved degree, complete a Professional Year, and pass the financial adviser exam

- Maintain at least 40 hours of CPD annually under licensee policy

- Apply Best Interests Duty (Corporations Act s961B) and the 12 Code of Ethics standards on every piece of personal advice

The adviser owns the client’s outcome. The paraplanner owns the technical build that supports it.

Paraplanner vs Financial Advisor: Key Differences

The cleanest way to draw the line is client-facing accountability vs technical execution.

| Factor | Paraplanner | Financial Advisor (Adviser) |

|---|---|---|

| Client contact | Rarely; back-office role | Direct relationship owner |

| Licensing | Not required to be on FAR | Must be on FAR; AFSL or AR |

| Education | Degree-qualified; no PY required | Approved degree + Professional Year + exam |

| Core output | SOA / ROA / strategy modelling | Recommendation + ongoing relationship |

| Compliance ownership | Drafts compliant documents | Signs and owns the advice |

| Best Interests Duty | Supports application | Legally responsible |

| Reports to | Adviser or paraplanning manager | Licensee or own AFSL |

A paraplanner is often more technically current on a complex strategy than the adviser they support, they spend their week deep in modelling and product research. But they don’t carry the licensing or the personal liability for the recommendation itself. That stays with the adviser.

Skills Comparison: Paraplanner vs Financial Advisor

The two roles draw on overlapping knowledge but very different skill emphases.

Paraplanner core skills:

- Strategy modelling across super, retirement, debt, and insurance

- Compliance writing, turning verbal strategy into defensible SOA prose

- Software fluency, XPLAN, Midwinter AdviceOS, COIN, IRESS

- Product and platform research (Netwealth, HUB24, BT Panorama, CFS Edge)

- Attention to detail under deadline pressure

Financial adviser core skills:

- Client discovery and goal setting

- Strategy formulation: knowing which levers to pull for which client

- Plain-English communication of tax, super, insurance, and investment trade-offs

- Behavioural coaching: keeping clients on plan through volatility

- Practice management and ongoing service delivery

The clearest signal: a paraplanner’s day is measured in files completed; an adviser day is measured in client meetings and relationships managed.

How Paraplanners and Financial Advisors Work Together

In a well-run practice, the paraplanner and adviser sit at opposite ends of the same workflow:

- Adviser meets the client, scopes goals, gathers fact-find data, and forms the strategy.

- Paraplanner builds the modelling, completes the research, and drafts the SOA against the licensee template.

- The adviser reviews, signs, and presents the advice, owning every recommendation in front of the client.

- Paraplanner prepares implementation paperwork, ROAs for ongoing reviews, and audit-ready file notes.

This is where outsourced paraplanning services earn their place. An Inside Advisor, an adviser working inside a busy practice, can free 10 to 15 hours a week by handing the technical drafting to an external paraplanning team. That’s time redirected to client conversations, business development, and the strategy work that compounds.

According to Adviser Ratings’ Australian Financial Advice Landscape report, adviser numbers on the Financial Advisers Register have fallen from over 28,000 in 2019 to roughly 15,500, and most remaining advisers cite capacity constraints as their top operational risk. Outsourced paraplanning is one of the few levers that lifts capacity without lifting compliance risk.

Why Outsourced Financial Planning Support Matters

For a practice running tight on capacity, outsourced financial planning support does three things:

- Buy back adviser time. The adviser stops drafting SOAs at 9pm and starts spending evenings with clients, prospects, or family.

- Creates a consistent compliance layer. An experienced outsourced paraplanner sees hundreds of files across multiple licensees. That breadth catches issues an internal team can miss.

- Scales capacity without headcount. Peak periods like EOFY, end-of-CPD-year, post-Federal Budget get absorbed without hiring or overtime.

The trade-off is that you lose some informal “next desk” collaboration. Good outsourced paraplanning teams compensate for structured intake, defined turnaround SLAs, and direct adviser-to-paraplanner communication channels, not a faceless ticketing queue.

Conclusion

The Paraplanner vs Financial Advisor question isn’t really a comparison; it’s a partnership. The adviser owns the client and the recommendation; the paraplanner owns the technical build and the compliant documentation. Practices that draw the line cleanly scale faster, spend less on rework, and run tighter on compliance.

For Inside Advisors juggling a full client load and back-office drafting, the question worth asking isn’t “do I need a paraplanner?”, it’s “should that paraplanner sit in my office, or at NCSGX ?”

How NCSGX Can Help

NCSGX provides outsourced paraplanning services to Australian advisers, dealer groups, and self-licensed practices, drafting SOAs and ROAs against your licensee templates, completing strategy and product research, preparing review packs, and absorbing peak workload through EOFY and review season without you adding headcount. Our team works across the major platforms (Netwealth, HUB24, BT Panorama, CFS Edge) and software environments (XPLAN, Midwinter AdviceOS, COIN), building every document to your house style and your licensee’s audit framework. If your SOAs are running long, your Review: Backlog is creeping, or you’re hesitating on new clients because the back-end can’t keep up, explore our outsourced paraplanning services to talk through how an outsourced paraplanning workflow would fit into your practice.

Frequently Asked Questions (FAQ)

1. Is a paraplanner the same as a financial adviser?

No. A paraplanner builds the technical advice document and modelling; the adviser is the licensed professional who recommends the strategy and owns the client’s relationship. A paraplanner does not need to be on ASIC’s Financial Advisers Register.

2. Can a paraplanner give financial advice in Australia?

Not personal advice to retail clients, that requires AFSL coverage as an adviser or Authorised Representative. A paraplanner provides technical and document support. The adviser is the one who signs off and presents the advice.

3. Do all financial advisors use paraplanners?

No, but most growing practices do, either in-house or outsourced. Sole practitioners sometimes draft their own SOAs early on, then outsource as the book grows past the point of self-drafting being viable.

4. What qualifications does a paraplanner need in Australia?

There’s no single mandatory licence. Most paraplanners hold a relevant degree (finance, commerce, financial planning) plus the Diploma or Advanced Diploma of Financial Planning. Some hold the same approved qualifications as advisers. Software literacy in XPLAN, Midwinter, or COIN is usually expected.

5. Is outsourced paraplanning compliant with Best Interests Duty?

Yes. BID applies to the licensed adviser, not the paraplanner. Provided the adviser reviews, signs, and owns the advice, outsourcing the drafting is a long-established and compliant practice.