USA

USA

Canada

Canada

Australia

Australia

The global minimum tax rules are no longer a future concern, they are an active compliance reality for thousands of multinational groups worldwide. As jurisdictions across Europe, Asia-Pacific, and beyond enforce their Pillar Two legislation, senior leaders must understand not just the mechanics but the strategic decisions these rules demand. At NCSGX, we have put together this guide to set out what every in-scope organization needs to know in 2026.

What Are the Global Minimum Tax Rules?

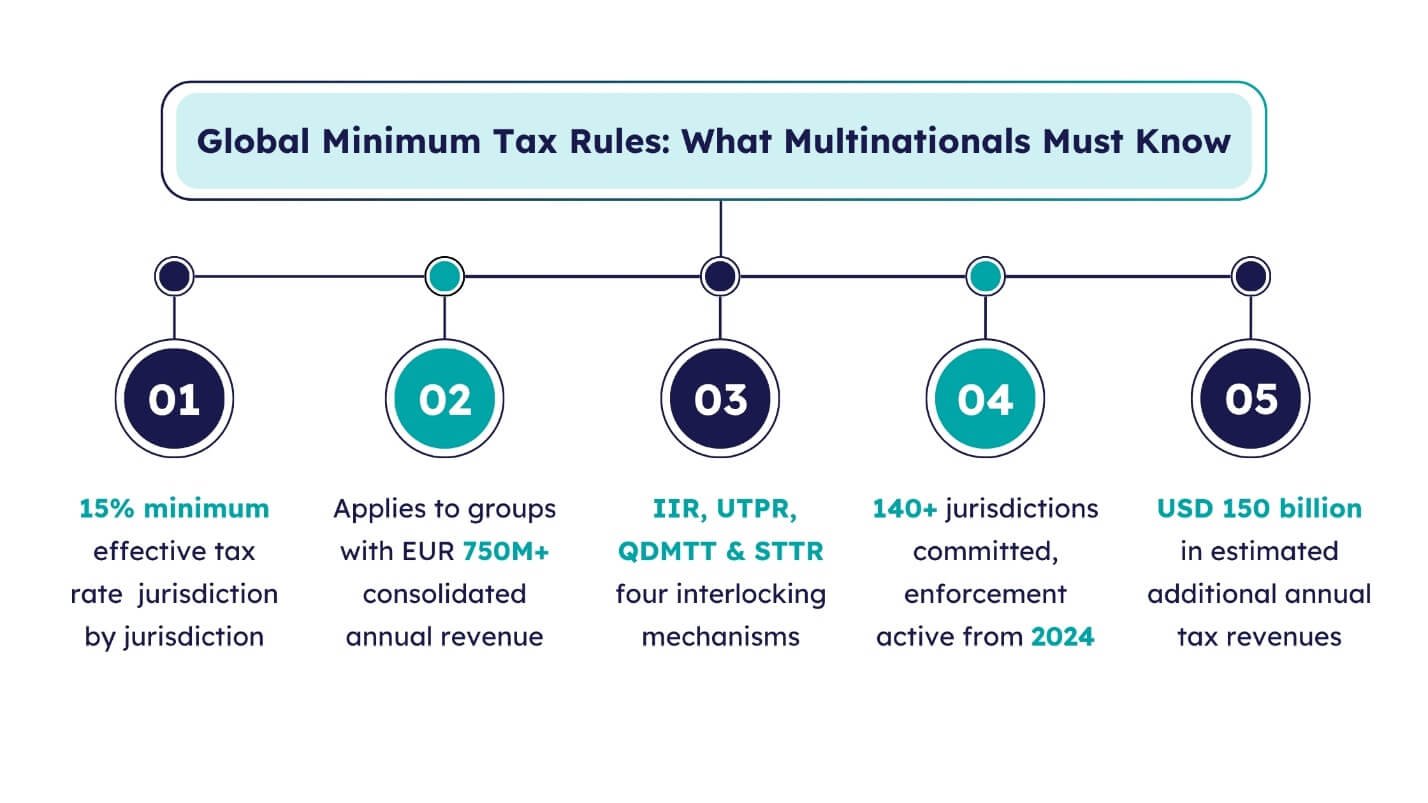

The global minimum tax rules, formally known as the OECD’s Pillar Two framework, establish a coordinated floor of 15% effective tax rate (ETR) on the profits of large multinational enterprise (MNE) groups, assessed jurisdiction by jurisdiction. Where a group’s effective rate in any country falls below 15%, a top-up tax is triggered to make up the difference.

These rules emerged from the OECD/G20 Inclusive Framework’s Two-Pillar Solution, designed to curtail profit shifting to low-tax jurisdictions and bring greater coherence to international corporate taxation. More than 140 jurisdictions have politically committed to the framework, and enactment is well underway, making this one of the most significant shifts in international tax policy in a generation.

The OECD estimates that the global minimum tax could raise approximately USD 150 billion in additional annual tax revenues globally.

The Four Core Mechanisms of Pillar 2 Rules

The Pillar 2 rules use interlocking mechanisms to ensure that low-taxed profits are captured somewhere in the group, regardless of where the parent or subsidiaries are located.

1. Income Inclusion Rule (IIR)

The IIR is the primary instrument of the framework. It operates at the level of the ultimate parent entity, requiring it to pay a top-up tax on its allocable share of low-taxed profits earned by its subsidiaries. Countries, including EU Member States, the UK, Japan, and Canada, have enacted IIR provisions effective from fiscal years beginning in 2024.

2. Undertaxed Profits Rule (UTPR)

The UTPR functions as a backstop to the IIR. Where the parent jurisdiction has not implemented an IIR or applies it only partially, the UTPR allows other jurisdictions where the group operates to deny deductions or make equivalent adjustments to collect residual top-up tax. Most jurisdictions are applying UTPR from 2025 or 2026.

3. Qualified Domestic Minimum Top-Up Tax (QDMTT)

A QDMTT allows a jurisdiction to collect top-up tax on its own low-taxed profits before foreign IIR or UTPR rules come into play. Where a QDMTT is aligned with GloBE standards, it generally reduces or eliminates the amount collectable under foreign mechanisms, preserving local tax revenue and offering greater certainty for in-country operations.

4. Subject to Tax Rule (STTR)

The STTR is a treaty-based rule allowing source jurisdictions to apply additional tax on specific intra-group payments, such as interest and royalties, where those payments are taxed below a 9% minimum rate in the recipient jurisdiction. It targets source-based taxing rights rather than consolidated ETR, complementing the broader GloBE framework.

OECD Global Tax: Where Implementation Stands in 2026

The OECD global tax implementation timeline has evolved significantly since the original political agreement in 2021. Here is where major blocs stand:

|

Jurisdiction |

IIR Effective |

UTPR Effective |

QDMTT |

|

EU Member States |

2024 |

2025 |

Most enacted |

|

United Kingdom |

2024 |

2025 |

Enacted |

|

Japan, South Korea, Australia |

2024 |

2025–2026 |

Enacted/in progress |

|

Canada |

2024 |

2025 |

Enacted |

|

Switzerland, UAE |

2024 |

2025 |

Enacted |

|

United States |

Partial alignment |

Not adopted |

— |

Legislative activity continues, with jurisdictions refining safe harbor provisions, administrative simplifications, and interactions with domestic minimum taxes through 2025 and 2026. Groups must maintain a live monitoring process across all relevant jurisdictions.

For authoritative, jurisdiction-level implementation updates, refer to the OECD Pillar Two implementation tracker and the KPMG Global Tax Legislative tracker.

Strategic Implications of the Global Minimum Corporate Tax

The global minimum corporate tax is not merely a technical tax matter. Its reach extends into business strategy, financial reporting, operating model design, and board-level governance. Organizations that treat Pillar Two purely as a compliance exercise will find themselves exposed.

Key strategic pressure points include:

- Increased tax cost and volatility: Groups with below-15% ETRs in any jurisdiction face incremental top-up taxes, compounded by deferred tax effects that can create earnings volatility quarter to quarter.

- Erosion of traditional low-tax structures: IP holding companies, financing entities, and regional hubs in low-tax jurisdictions are now directly exposed where residual profits attract top-up taxes elsewhere in the group.

- Degraded value of tax incentives: Non-refundable credits, holidays, and preferential regimes that reduce local ETR may trigger top-up taxes in other jurisdictions, partially neutralizing the return on real investment decisions.

- Heightened data and systems demand: Globe calculations require granular, reconciled data linking accounting profit to tax attributes on a jurisdiction-by-jurisdiction basis, a level of detail most group reporting infrastructures were not designed to produce.

- Investor and stakeholder scrutiny: Pillar Two disclosures will give investors, lenders, and tax authorities far greater transparency over effective tax rates and profit allocation, raising the bar on tax risk governance.

Priority Actions for Tax and Finance Leaders

Leading organisations are approaching Pillar Two as a multi-year transformation programme. The following actions reflect current best practice and the NCSGX framework for groups seeking to manage risk and protect value:

- Conduct a structured impact assessment:Map the group entity structure,identify all in-scope jurisdictions, and model jurisdictional ETRs across business and legislative scenarios, including M&A activity, restructuring, and changes in incentive eligibility.

- Close the data gap:Assess the distance between current tax reporting capabilities andGloBE requirements. Many groups find that entity-level accounting data, deferred tax schedules, and covered-tax records are not integrated in a way that supports efficient Pillar Two calculation.

- Invest in technology-enabled workflows:Build or adapt ERP, consolidation, and tax reporting tools to capture,validate, and store Pillar Two data on an ongoing basis. Manual approaches are not sustainable on scale.

- Revisit structures and incentive strategies:Re-evaluate holding, financing, IP, and supply-chain structures with Pillar Two ETRs in view. Engage proactively with hostjurisdictions where investment decisions depend on incentives that may now be partially neutralised.

- Embed Pillar Two in governance frameworks:Define roles, responsibilities, controls, and escalation protocols across tax, finance, legal, and business functions. Brief boards and audit committees on the expected ETR trajectory and disclosure obligations.

- Establisha legislative monitoring process: Safe harbour rules, administrative guidance, and country-specific interpretations continue to evolve. A structured tracking process across all relevant jurisdictions is now a baseline compliance requirement, not an optional enhancement.

The Bottom Line

The global minimum tax rules represent a structural reset in how large multinational businesses are taxed. For in-scope groups, the question is no longer whether Pillar Two applies, it is how thoroughly the organisation has assessed its exposure and built the capabilities to comply.

The groups that act with urgency and rigor now will be better placed to manage cost, protect value, and maintain stakeholder confidence as this framework becomes the permanent backdrop to international business.

To understand how NCSGX can support your Pillar Two readiness from impact assessment to systems design and governance, get in touch with our team today.

How NCSGX can help

NCSGX helps multinational groups turn Pillar Two from a compliance challenge into a managed business process. Our team supports organisations at every stage of readiness, from impact assessment and jurisdictional modelling to data gap analysis, process design, technology enablement, and governance support.

By combining technical tax expertise with practical implementation experience, we help clients build the controls, workflows, and visibility needed to stay compliant, reduce risk, and make informed strategic decisions in a rapidly changing global tax environment.