USA

USA

Canada

Canada

Australia

Australia

Most people are surprised to learn that Canada has no inheritance tax, and that misunderstanding can cost them significantly. Whether you’re a Canadian resident receiving an estate, a non-resident inheriting Canadian property, or a dual citizen navigating assets on both sides of the border, canada inheritance tax rules are more nuanced than they appear.

In 2026, cross-border tax obligations between Canada and the United States have become an even sharper concern. With evolving U.S. estate tax thresholds and ongoing CRA scrutiny of cross-border asset transfers, getting this wrong isn’t just an inconvenience; it can trigger unexpected tax bills, compliance penalties, and costly delays in estate administration.

This guide breaks it all down clearly, so you can plan rather than react after the fact with NCSGX Canada.

Does Canada Have an Inheritance Tax?

The short answer: no, Canada does not have a formal inheritance tax. Beneficiaries do not pay tax on assets they receive from an estate. There is no estate taxes levied at the federal or provincial level, unlike in the United States, where estate taxes can apply on assets above a certain threshold.

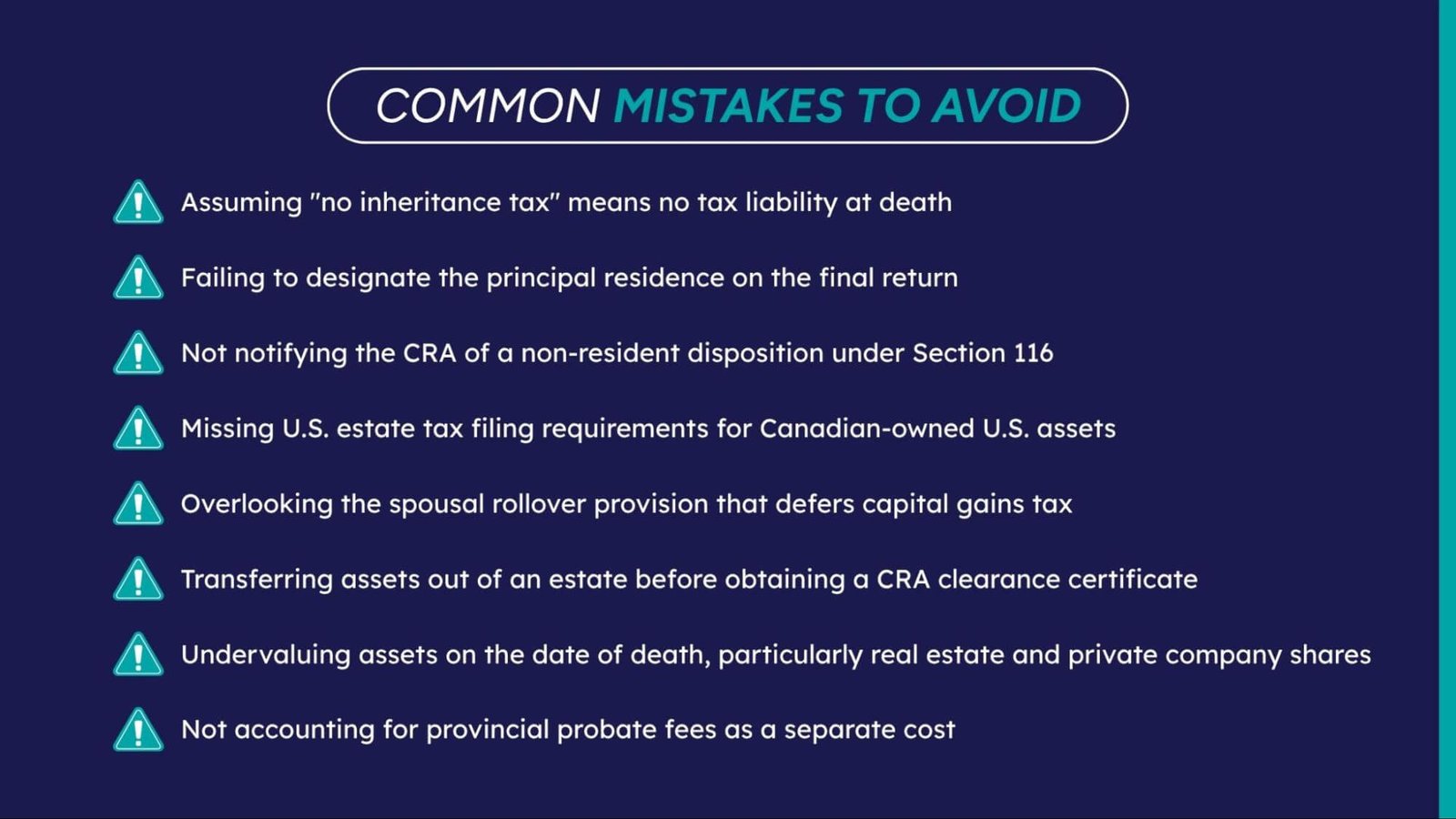

However, “no inheritance tax” does not mean “no tax at death.” This is where the deemed disposition rule changes everything.

When a person passes away, the Canada Revenue Agency (CRA) treats them as if they sold all their assets at fair market value on the date of death. This “deemed disposition” can trigger significant capital gains tax on the final tax return, and the estate, not the beneficiary, pays that tax.

How Inheritance Is Taxed in Canada

While beneficiaries receive assets tax-free, the estate itself bears the tax burden. The executor of the estate must file a final T1 income tax return (and potentially additional optional returns) on behalf of the deceased for the year of death.

Key responsibilities include:

- Calculating any income earned up to the date of death

- Reporting capital gains from the deemed disposition of all non-exempt assets

- Claiming any available deductions, including the principal residence exemption

- Paying all taxes owed before distributing assets to beneficiaries

The estate cannot close, and assets cannot be transferred, until the CRA issues a clearance certificate confirming all taxes have been paid or secured.

Capital Gains Inheritance Canada

Under Canada’s capital gains inheritance rules, the estate pays tax on 50% of the capital gain, though note that the 2024 federal budget proposed increasing the inclusion rate to two-thirds for gains above $250,000. The status of this proposal should be confirmed with a tax advisor for 2026 filings.

Inheritance Tax Canada on Property

Real estate is often the most valuable and most complicated asset in an estate.

Principal residence: If the deceased lived in the home as their primary residence throughout their ownership, the principal residence exemption (PRE) may fully shield the capital gain from tax. Proper designation and documentation are essential.

Investment or rental property: No PRE is available. The full capital gain is subject to deemed disposition rules and can generate a substantial tax bill.

Vacation and foreign property: Canadian residents are taxed on worldwide assets at death, including U.S. vacation homes, foreign investment accounts, and overseas real estate. This is where cross-border tax exposure becomes significant.

Inheritance Tax in Canada for Non-Residents

Inheritance tax in Canada for non-residents adds a layer of complexity that many overlook until they’re already in the middle of administering an estate.

When a non-resident inherits or disposes of Canadian situs assets, property physically located in Canada, such as real estate or shares of private Canadian corporations, they face:

- Section 116 withholding tax of 25% on the gross sale price (or 50% if the property is depreciable)

- A mandatory requirement to notify the CRA before or immediately after the disposition

- Potential penalties for non-compliance, even if no net gain is realised

Non-residents must apply for a Certificate of Compliance from the CRA. Buyers of Canadian property from non-residents are legally required to withhold tax on the purchase price unless this certificate is received. Missing this step can result in the buyer becoming personally liable.

Cross-Border Tax Rules 2026

This is where Canada’s inheritance tax meets its most complex counterpart: the U.S. estate tax.

U.S. Estate Tax Exposure for Canadians

Americans and U.S. residents aren’t the only ones exposed to the U.S. estate tax. Canadian residents who own U.S. situs assets, including U.S. real estate, U.S. stocks held directly, or U.S.-based business interests, may face U.S. estate tax at death, regardless of their citizenship.

In 2026, the U.S. estate tax exemption is significant but not unlimited. For Canadians who own U.S. assets, the exposure depends on the value of those assets relative to the full estate. This is governed by the Canada – U.S. Tax Treaty, which provides a pro-rated exemption, but only if the proper election is made on a U.S. estate tax return.

Double Taxation Risks

Without careful planning, both Canada and the U.S. may tax the same asset at death:

- Canada imposes capital gains tax under deemed disposition

- The U.S. may levy estate tax on the same U.S. situs asset

The treaty provides a foreign tax credit mechanism to prevent double taxation, but accessing it requires accurate, timely filing in both countries.

Filing Requirements in 2026

- Canada: Final T1 return, CRA clearance certificate, possible T3 trust return

- U.S.: Form 706-NA (U.S. estate tax return for non-resident aliens), Form 8833 (treaty election)

- Deadlines: U.S. Form 706-NA is due 9 months after the date of death (15-month extension available)

Tax Planning Strategies

Proactive planning is the most effective tool available to estates with cross-border complexity.

Spousal rollovers: Assets transferred to a surviving Canadian spouse can defer capital gains tax until the surviving spouse disposes of the asset or passes away.

Alter ego and joint partner trusts: These allow individuals 65 and older to transfer property into a trust during their lifetime, bypassing probate and potentially controlling the timing of capital gains.

Gifting strategies: Transferring appreciated assets during your lifetime triggers deemed disposition at the time of the gift but combined with lifetime exemptions and income-splitting opportunities, gifting can reduce overall estate tax exposure.

Life insurance: A well-structured permanent life insurance policy can provide a tax-free death benefit to cover capital gains tax at death, ensuring liquidity without forced asset sales.

Cross-border asset structuring: For Canadians with U.S. holdings, holding U.S. real estate through a Canadian corporation or trust can reduce exposure to U.S. estate tax, though this must be balanced against other tax consequences.

Quick Comparison Table

Scenario | Tax Type | Who Pays | Key Risk |

Canadian resident dies with RRSP | Income tax (full value) | Estate | No spousal rollover if no eligible beneficiary |

Principal residence inherited | None (if PRE claimed) | Estate (admin cost only) | Missing the PRE designation deadline |

Rental property inherited | Capital gains tax | Estate | High tax on large accrued gains |

Non-resident sells inherited Canadian property | Withholding tax (25%) | Non-resident seller | Buyer liability if cert. missed |

Canadian with U.S. real estate | U.S. estate tax + Canada capital gains | Estate | Double taxation without a treaty election |

TFSA at death | Tax-free to the beneficiary | N/A | Tax on income earned after death |

Conclusion

Canada’s inheritance tax landscape in 2026 is deceptively complex. Deemed disposition, capital gains exposure, withholding rules for non-residents, and cross-border U.S. estate tax obligations all intersect and getting any one of them wrong can be costly.

Whether you’re an executor, a non-resident with Canadian property, or a high-net-worth individual planning your estate, expert guidance is essential.

Speak to a cross-border tax expert today. Book your consultation with NCSGX

How NCSGX Canada Can Help You

NCSGX Canada is a specialised cross-border tax firm helping Canadians, non-residents, and expats navigate the complexities of inheritance, estate planning, and Canada – U.S. tax obligations. Whether you’re an executor managing a final return, a non-resident dealing with Canadian property, or a high-net-worth individual with assets on both sides of the border, we bring the expertise to keep you compliant and tax-efficient. Our team handles everything from CRA clearance certificates and Section 116 filings to full cross-border estate structures, so nothing falls through the cracks.