USA

USA

Canada

Canada

Australia

Australia

T3 Trust Return Guide: Step-by-Step Filing for Trustees in 2026

If you’re administering a trust in Canada, the T3 trust return guide isn’t optional reading; it’s your compliance lifeline. The Canada Revenue Agency has significantly tightened reporting requirements over the past few years, and 2026 brings its own set of nuances that every trustee, CPA, and financial decision-maker needs to understand before the deadline hits.

Whether you’re handling an estate trust, a family trust, or an inter vivos arrangement, getting the T3 right matters, both legally and financially.

What Is a T3 Return and Who Must File One?

The T3 Return, formally known as the T3 Trust Income Tax and Information Return, is the annual tax filing required for most trusts resident in Canada. It reports income earned by the trust and any amounts allocated to beneficiaries.

Trustees managing trusts alongside incorporated entities should also understand how corporate tax obligations differ from trust filings, particularly when handling a T2 corporate tax return and broader CRA compliance requirements.

Trusts required to file a T3 include:

- Testamentary trusts (including graduated rate estates)

- Inter vivos trusts

- Employee benefit plan trusts

- Retirement compensation arrangements

- Certain bare trusts (updated rules apply post-2023)

A common misunderstanding is that a trust with no income doesn’t need to file. That’s not always accurate. Since the 2023 amendments, even bare trusts with no activity may have reporting obligations under the expanded beneficial ownership rules.

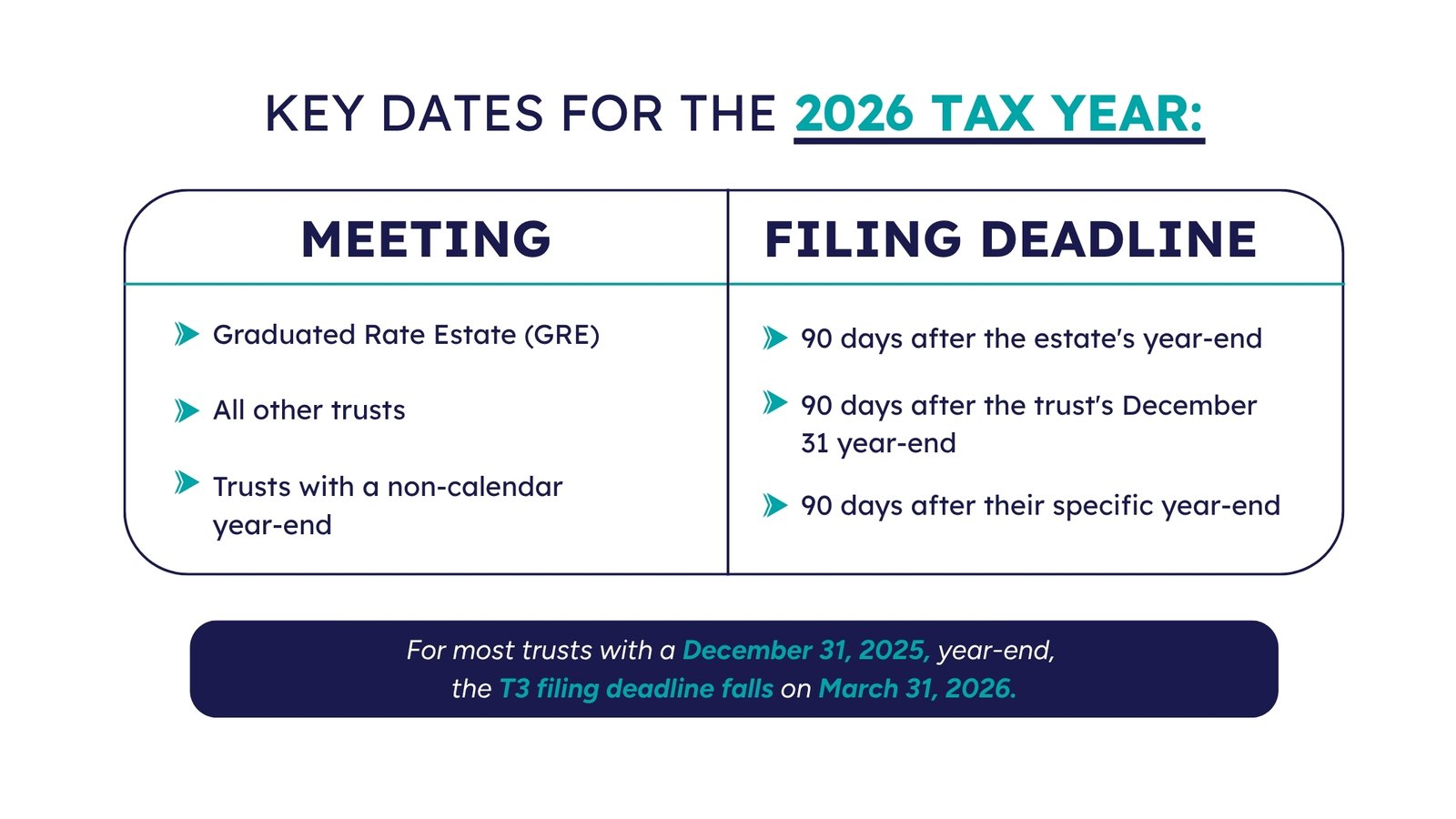

2026 Filing Deadlines: What Trustees Must Know

Timing is everything in trust administration. Missing a T3 deadline doesn’t just mean a late-filing penalty, it can cascade into compliance reviews and trustee liability.

Slippage here is costly. The CRA charges a late-filing penalty of $25 per day, with a minimum of $100 and a maximum of $2,500. For trusts subject to the expanded reporting requirements, gross negligence penalties can go much higher.

Step-by-Step Guide to Filing a T3 Return

Filing a T3 return involves considerably more moving parts than a personal or corporate return. Here’s a structured walkthrough to keep your process clean and defensible.

Step 1: Confirm Trust Residency and Filing Obligation

Establish whether the trust is resident in Canada and whether a filing obligation exists. Review the trust deed, the location of trustees, and the nature of trust assets.

Step 2: Determine the Trust’s Year-End

Most trusts use a December 31 year-end, but certain trusts, particularly GREs, may have a different fiscal period. Confirm this before proceeding.

Step 3: Gather Trust Income Information

Collect all income earned within the trust during the tax year:

- Investment income (interest, dividends, capital gains)

- Rental income

- Business income (if applicable)

- Foreign income requiring conversion and reporting

The CRA’s T4013 publication is the authoritative guide here and should be your primary reference for line-by-line completion.

Step 4: Calculate Allocations to Beneficiaries

Income that is paid or payable to beneficiaries during the year can generally be deducted from the trust’s taxable income and instead taxed in the beneficiaries’ hands. This allocation must be documented carefully.

Issue T3 slips to each beneficiary showing their share of income by type (interest, dividends, capital gains, etc.).

Step 5: Complete the T3 Return Schedules

The T3 return includes multiple schedules depending on your trust’s situation:

- Schedule 1: Dispositions of Capital Property

- Schedule 2: Reserves on Dispositions

- Schedule 8: Investment Income, Interest, and Penalties

- Schedule 9: Calculation of Trust’s Income Allocations

- Schedule 11: Subsidiary Corporations

Don’t skip schedules that appear irrelevant. An incorrectly omitted schedule can trigger a review.

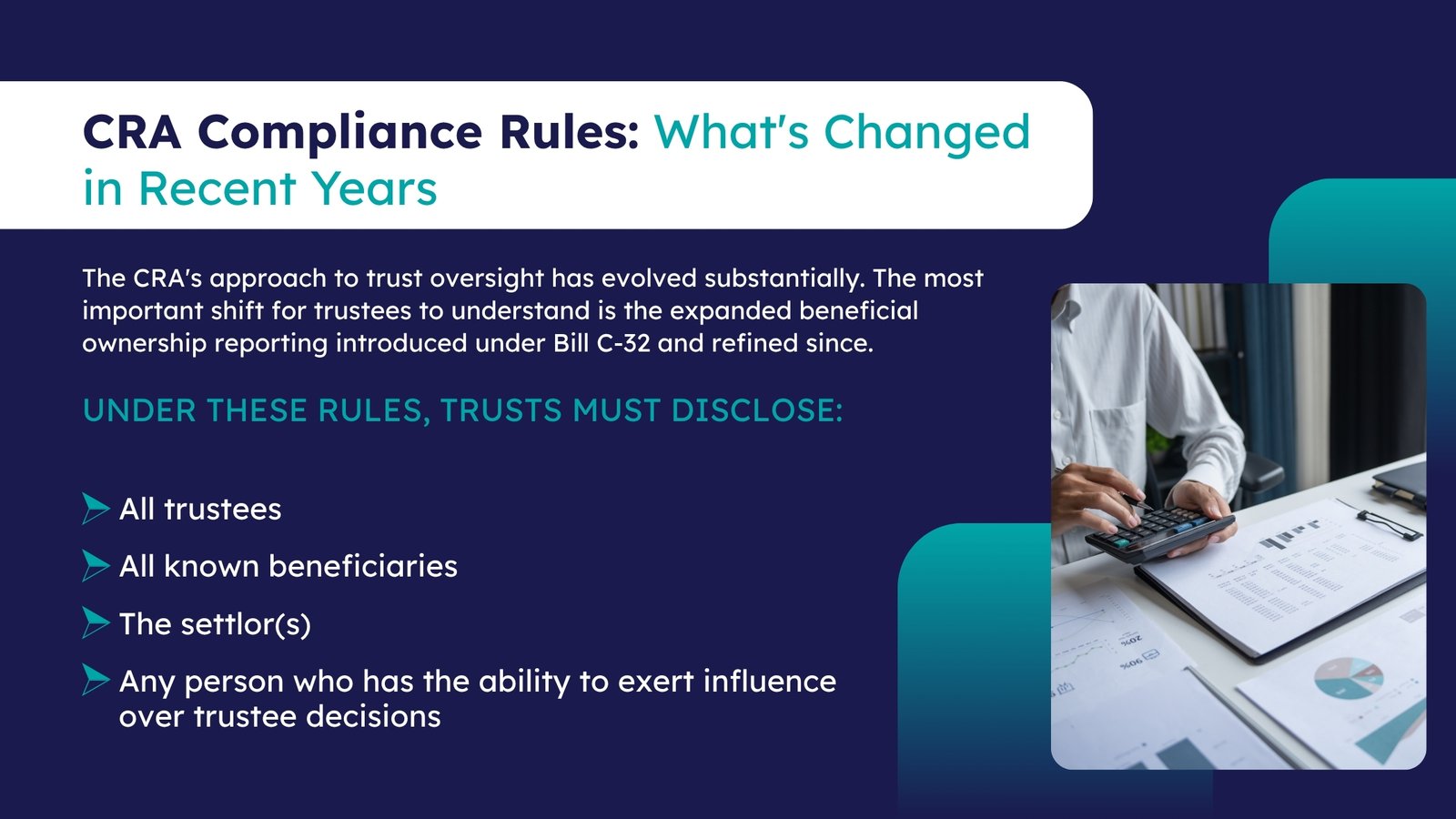

Step 6: Complete the Beneficial Ownership Schedule (If Required)

Since the CRA expanded trust reporting rules effective for 2023 and onward, most trusts must now report beneficial owners, settlors, trustees, and beneficiaries, even if the trust had no income. This is one of the most significant compliance shifts in recent Canadian trust law.

For a deeper breakdown of what this means practically, ClearEstate’s T3 Trust Return guide offers a practical supplementary perspective on navigating these changes.

Step 7: File Electronically or by Mail

Trusts with more than $1 million in assets are required to file electronically. For smaller trusts, CRA accepts paper filing, though electronic submission through authorized tax software is generally faster and creates a cleaner audit trail.

Failure to comply isn’t just a minor administrative issue. Penalties for non-compliance with the expanded reporting rules can reach $2,500 per failure, and intentional evasion can attract gross negligence penalties of 5% of the maximum value of trust property.

For trustees handling complex reporting obligations, working with experienced business tax services professionals can significantly reduce compliance risk and improve filing accuracy.

For additional guidance on T3 trust income tax obligations and what CRA expects, TurboTax Canada’s overview provides a digestible breakdown useful for clients and junior team members you may be briefing.

Trustee Responsibilities and Personal Liability

One thing many trustees underestimate is their personal exposure. Acting as a trustee is a fiduciary role with real legal and financial consequences.

As a trustee, you are responsible for:

- Filing the T3 return accurately and on time

- Remitting any tax payable

- Maintaining proper records for at least six years

- Notifying CRA of changes to trustee status or trust structure

If the trust fails to pay its tax liability and the CRA cannot collect from trust assets, trustees can be held personally liable under Section 159 of the Income Tax Act. This is not a theoretical risk, it has been enforced.

This is precisely why many trustees and estate administrators work with professional advisors. If you’re managing multiple trusts or complex estate structures, our professional services team can provide hands-on compliance support.

Common Mistakes Trustees Make on T3 Returns

Even experienced professionals make errors on T3 filings. Here are the most recurring ones:

- Missing the expanded beneficial ownership disclosure:Many trustees filed for years without this, and the 2023-onward rules created a significant compliance gap for those whodidn’t update their practices.

- Incorrectly classifying the trust type:Misidentifying a GRE versus a testamentary trust that has passed its 36-month windowresults in incorrect tax rate application.

- Failing to issueT3 slips to beneficiaries on time: T3 slips must reach beneficiaries by the last day of March. Late slips create downstream problems for beneficiaries filing their personal returns.

- Not reporting foreign assets held in trust:If the trust holds foreign property exceeding $100,000 CAD, a T1135 (Foreign Income Verification Statement) may also berequired.

- Using outdated trust deeds as a complianceguide:Trust deeds often don’t reflect current CRA requirements. Always layer the current Canada Revenue Agency T3 trust return rules on top of what the deed says.

Conclusion

The T3 trust return guide landscape in 2026 is more demanding than ever. Between expanded beneficial ownership reporting, tightening deadlines, and heightened CRA enforcement, trustees cannot afford a reactive approach. Understanding your obligations under canada revenue agency T3 trust return rules isn’t just about avoiding penalties, it’s about protecting the beneficiaries you serve and the integrity of the trust structure itself.

If there’s any uncertainty about your filing position this year, now is the time to seek qualified guidance.

Ready to simplify your T3 filing process? Contact our team today and get expert support before the deadline.

How NCSGX Can Help

Navigating the cra t3 trust guide requirements on your own, especially with expanded reporting and tightening CRA scrutiny, is a significant undertaking. At NCSGX, we work directly with trustees, estate executors, CPAs, and family offices across Canada to manage T3 compliance from start to finish.

From initial trust classification to beneficial ownership disclosure, beneficiary slip preparation, and CRA correspondence, we handle the complexity so you can focus on broader fiduciary and strategic responsibilities.

Explore our full range of financial compliance services