USA

USA

Canada

Canada

Australia

Australia

Introduction

Many business owners associate an IRS notice with audits or serious tax problems. In reality, many notices are generated because of routine bookkeeping errors, such as reporting mismatches, missed income, payroll mistakes, or inaccurate deductions. Even small recordkeeping issues can create discrepancies that prompt the IRS to request clarification.

Accurate bookkeeping helps ensure your financial records, payroll reports, and tax filings stay consistent throughout the year. At NCSGX, we work with businesses to maintain organized, tax-ready books that support better compliance and informed financial decisions. Understanding the bookkeeping errors that trigger IRS notices can help you identify potential issues early and reduce the risk of avoidable IRS correspondence.

Key Takeaways

- Small bookkeeping errors often create reporting mismatches that may prompt an IRS notice.

- Regular reconciliations help identify duplicate entries, missing transactions, and inaccurate balances before tax filing.

- Payroll taxes, contractor reporting, and deductible expenses require careful documentation throughout the year.

- Accurate books make it easier to respond to IRS inquiries with supporting records.

Businesses that want to understand how to avoid IRS notices bookkeeping issues should focus on timely reconciliations, accurate payroll reporting, and consistent tax documentation.

Bookkeeping Errors That Trigger IRS Notices

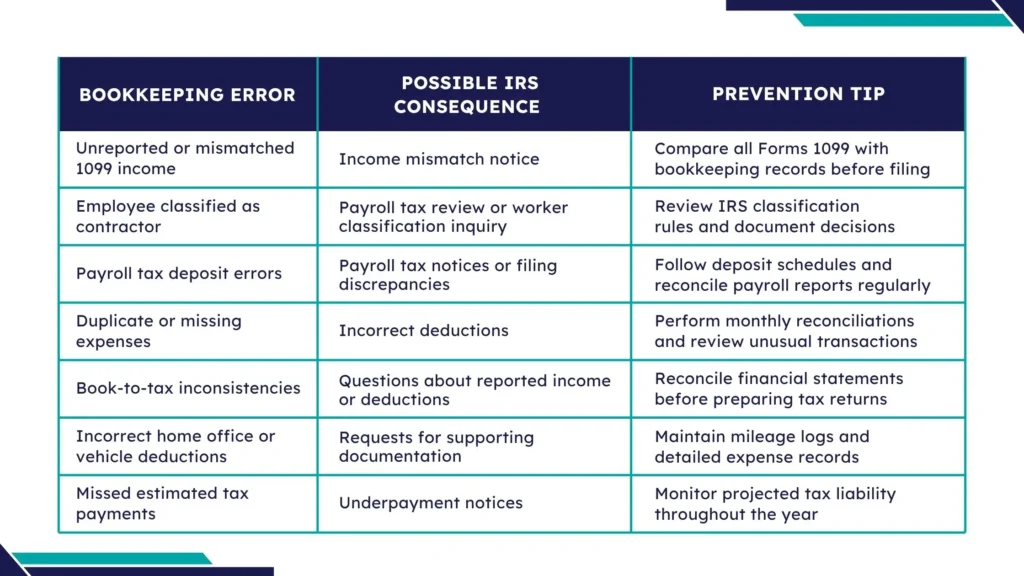

Bookkeeping errors that trigger IRS notices are often ordinary recordkeeping mistakes, not signs of fraud. A missed 1099, a payroll deposit made on the wrong date, or a return that does not match the books can be enough to create an IRS mismatch notice.

The IRS relies heavily on information returns and tax filings that should line up with one another. When the numbers do not reconcile, the IRS may send a notice asking for clarification, a correction, or payment, even if the underlying issue is only a bookkeeping error. These are among the common bookkeeping mistakes IRS systems identify during automated matching reviews. Even businesses with accurate operations can receive notices when routine bookkeeping records contain inconsistencies.

Common Bookkeeping Errors and Their Potential IRS Impact

Unreported or Mismatched 1099 Income

One of the most common bookkeeping errors that trigger IRS notices involves reporting income that does not match the information received by the IRS from customers or payment processors. An income mismatch IRS notice is commonly generated when the income reported on a tax return does not match the amounts reported on Forms 1099 or other information returns.

When a business issues Form 1099-NEC or Form 1099-MISC, the IRS receives the same information. Businesses can review the IRS Instructions for Forms 1099 to understand reporting requirements and reduce the risk of reporting mismatches. If your tax return reports less income than those forms indicate, the IRS’s automated matching system may generate a notice.

Common reasons for mismatches include:

- Forgetting to record a customer payment

- Recording income in the wrong tax year

- Duplicate customer accounts in accounting software

- Failing to reconcile deposited payments with issued 1099s

For example, a consulting firm may receive several Forms 1099-NEC from different clients. If one payment is accidentally omitted during year-end bookkeeping, the tax return may report less income than the IRS expects.

Misclassifying Employees as Independent Contractors

Worker classification continues to receive significant IRS attention because it directly affects payroll tax obligations.

Employees generally receive wages subject to payroll tax withholding, while independent contractors are responsible for paying their own self-employment taxes. Treating an employee as a contractor without meeting IRS criteria can lead to payroll tax reporting issues and additional review.

Some common warning signs include:

- Controlling when and how someone performs their work

- Providing ongoing supervision similar to employees

- Supplying all equipment while maintaining long-term working arrangements

If worker classification is unclear, businesses can review the IRS guidance on Employee versus Independent contractor status or request a determination by submitting Form SS-8.

Payroll Tax Deposit Errors

Payroll tax reporting errors often begin with late or incorrect payroll tax deposits. Even if payroll is recorded accurately, deposits that don’t match Form 941 or Form 944 filings can trigger IRS notices.

These issues commonly arise when payroll is managed separately from bookkeeping or payroll schedules aren’t updated correctly. Businesses using professional Payroll Services can reduce these risks by keeping payroll records, tax deposits, and financial reporting aligned. Regular payroll reconciliations and following IRS guidance for employment tax deposits help maintain compliance. Regular reviews of payroll records can help identify payroll tax reporting errors before quarterly filings are submitted to the IRS.

Duplicate or Missing Expense Entries

Expense tracking errors affect more than internal financial reporting. They can also create inaccurate deductions on tax returns.

Duplicate entries may overstate deductible expenses, while missing transactions can distort financial statements and taxable income.

Common causes include:

- Importing bank transactions multiple times

- Recording the same vendor invoice twice

- Missing receipts or invoices

- Posting transactions to incorrect accounts

Many of these issues stem from reconciliation errors tax records fail to identify before year-end financial statements are prepared.

For instance, a business owner manually enters a software subscription expense and later imports the same bank transaction through accounting software. Without proper review, both entries remain in the books, overstating deductions.

Inconsistent Reporting Between Books and Tax Return

Financial statements and tax returns should tell the same overall financial story, even though certain accounting adjustments may legitimately create differences.

Problems arise when bookkeeping records are incomplete or adjustments are overlooked during tax preparation.

Examples include:

- Revenue reported in financial statements but omitted from tax returns

- Incorrect year-end adjusting entries

- Inventory balances that do not match supporting records

A retailer may accurately record all sales throughout the year but forget to include a year-end inventory adjustment before filing taxes. The financial statements and tax return may then report different gross profit figures, creating questions during an IRS review. Consistent monthly reconciliations help reduce reconciliation errors tax records may otherwise carry forward into tax filings.

Accurate financial reporting begins with consistent bookkeeping throughout the year rather than last-minute corrections. Businesses that rely on professional Bookkeeping Services are often better positioned to identify reporting inconsistencies before tax filing deadlines arrive.

Incorrect Home Office or Vehicle Deduction Calculations

Home office and business vehicle deductions remain legitimate tax benefits for qualifying businesses. However, they require thorough documentation.

Many IRS notices arise not because these deductions are claimed, but because supporting records cannot substantiate them.

Suppose a consultant drives to client meetings throughout the year but reconstructs mileage from memory several months later. The estimates may differ from actual travel, making it difficult to support the deduction if questioned.

Missing or Late Estimated Tax Payments

Many self-employed individuals, partnerships, and certain business owners must make estimated tax payments during the year.

Bookkeeping problems can make these payments difficult to estimate accurately.

For example, if income is understated because invoices have not been recorded, estimated tax calculations may also be understated. Later, once the books are corrected, the actual tax liability may be higher than expected.

Cash flow planning plays an important role here. Businesses that review financial statements quarterly can often identify changing income trends early enough to adjust estimated tax payments accordingly.

What To Do If You Receive an IRS Notice

Receiving an IRS notice does not automatically mean you owe additional tax or made a serious mistake. Many notices simply request clarification or supporting documentation.

If you receive one:

- Read the Notice Carefully

- Compare the Notice with Your Records

- Respond Promptly

- Correct Bookkeeping Errors

- Consult a Tax Professional When Needed

The IRS guidance on notices provides explanations for many common notice types, while SCORE small business resources offer educational materials that help business owners improve financial management practices.

Conclusion

Most IRS notices begin with ordinary bookkeeping issues rather than intentional misconduct. Reviewing your records regularly, reconciling accounts, documenting deductions, and keeping payroll and tax filings consistent can significantly reduce compliance risks.

Understanding the bookkeeping errors that trigger IRS notices help businesses identify problems before they become costly distractions. For many small businesses, learning how to avoid IRS notices bookkeeping problems begins with maintaining organized records throughout the year rather than correcting them at tax time. If you need guidance in keeping your books IRS-ready, contact our team to learn how professional bookkeeping support can help reduce compliance risks.

How NCSGX Can Help

At NCSGX, we help businesses maintain accurate bookkeeping, payroll records, account reconciliations, and tax-ready financial statements throughout the year. Our team focuses on identifying reporting inconsistencies early, improving record accuracy, and supporting businesses with reliable financial information that helps simplify tax compliance and reduce the risk of IRS-related bookkeeping issues.

Frequently Asked Questions (FAQ)

1. Does every bookkeeping error trigger an IRS notice?

No. Many bookkeeping errors go unnoticed. However, mistakes that create reporting mismatches, missing income, or payroll discrepancies are more likely to result in an IRS notice. One of the most frequent examples is an income mismatch IRS notice, which occurs when third-party income reports differ from the amounts reported on the tax return.

2. How far back can the IRS flag bookkeeping mismatches?

The IRS may review prior tax years if it identifies discrepancies. The exact period depends on the type of issue and the applicable IRS rules.

3. Can fixing my books after receiving a notice reduce penalties?

It can help in some cases. Correcting your records promptly and responding accurately may resolve the issue, though whether penalties are reduced depends on your specific circumstances.

4. What bookkeeping mistakes are most likely to trigger IRS notices?

Common triggers include income mismatches, payroll reporting errors, duplicate deductions, and unreconciled financial records. Businesses should pay particular attention to payroll tax reporting errors, since even small filing discrepancies can result in IRS correspondence.

5. How can businesses reduce the risk of IRS bookkeeping issues?

Keep accurate records, reconcile accounts regularly, review tax filings carefully, and maintain supporting documents throughout the year.

6. Should I contact a tax professional after receiving an IRS notice?

If the notice involves complex tax issues or you are unsure how to respond, consulting a qualified tax professional can help you address it correctly and on time.

Rahul Sharma

Rahul Sharma is a Chartered Accountant with over 7+ years of experience in global accounting, bookkeeping, tax preparation, financial reporting, and compliance. At NCSGX, he leads accounting outsourcing operations, manages client engagements, and drives process improvements for international businesses. Through his writing, Rahul shares practical insights on accounting, outsourcing, taxation, and business finance, helping firms and professionals make informed financial and operational decisions.

All Posts