USA

USA

Canada

Canada

Australia

Australia

For paraplanners working alongside Australian financial advisers, the Annual Fee Consent and FDS Checklist sits at the centre of every ongoing fee renewal that crosses the desk. The Delivering Better Financial Outcomes (DBFO) reforms that commenced in January 2025 didn’t make this work disappear, they consolidated some documents, tightened others, and shifted the practical compliance burden onto the single annual consent that now does the job two separate documents used to.

This guide walks through what the consolidated regime looks like in practice, the ASIC guidelines for fee disclosure statements that still drive surveillance, and the annual fee consent compliance checklist a paraplanner can run before any consent leaves the office.

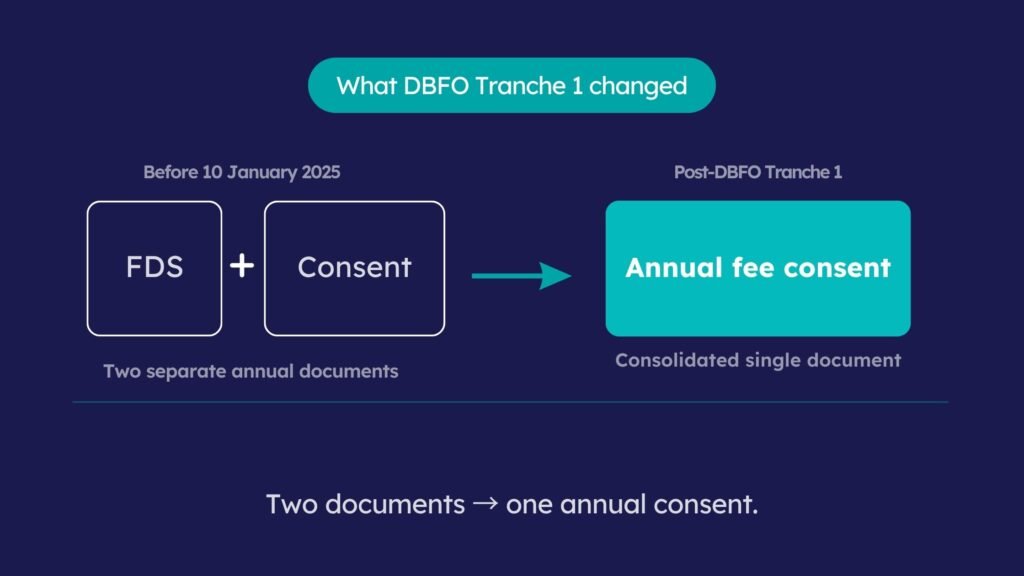

What DBFO Tranche 1 changed about FDS and consent

Before 10 January 2025, an ongoing fee client typically received two separate documents each year. The Fee Disclosure Statement (FDS) covered the historical disclosure of fees received and services provided over the previous 12 months. The written consent added by the post-Hayne Royal Commission reforms in July 2021 was the separate authority that allowed the licensee to deduct fees from the client’s product accounts. Anniversary dates, signed consents, and opt-in renewals: three moving parts that frequently fell out of sync.

The Treasury Laws Amendment (Delivering Better Financial Outcomes and Other Measures) Act 2024 collapsed these into a single annual document: the Ongoing Fee Consent. The consolidated form must still include the historical fee and service disclosures that used to live in the FDS, plus the forward-looking consent for the next 12 months. ASIC’s Information Sheet 286 (INFO 286) sets out how the regulator expects this to look into practice.

Practices with arrangements entered before 10 January 2025 had transitional provisions to migrate. By mid-2026, the bulk of advice practices have moved every client across to the new single-form template.

What the consolidated consent must contain

The single consent is doing two jobs at once. The Corporations Act, the Corporations Regulations 2001, and ASIC’s guidance set out the minimum content:

- The name and contact details of the fee recipient (the AFSL holder or authorised representative)

- The services the client received in the previous 12 months

- The fees the client was charged in the previous 12 months

- The services the client will be entitled to receive in the next 12 months

- The fees the client will be charged in the next 12 months, either as a stated dollar amount or a reasonable estimate with the calculation method

- The frequency and timing of fee deductions

- The account or accounts from which fees will be deducted

- Express client consent, with a date and a signature (or a verifiable electronic equivalent)

- Information about the client’s right to withdraw consent at any time

The forward-looking fee estimate is where most file errors creep in. If the fee is percentage-based or FUM-linked, the paraplanner needs evidence of the calculation methodology and the assumed account balance or growth assumption sitting behind it.

Paraplanner compliance checklist for FDS and ongoing fee consent

Before the consent goes back to the adviser for sign-off, the paraplanner is the second set of eyes. Working through this checklist on every file catches the majority of the issues ASIC has historically raised in surveillance reviews.

- Anniversary date alignment.Confirm thatthe consent of renewal date matches the original arrangement date (or the agreed annual review date documented in the Ongoing Service Agreement). A consent that’s been left to drift past the anniversary window is past the regulatory cut-off and the licensee’s deduction authority lapses with it.

- Services-rendered evidence.For every service listed as “delivered” in the prior 12 months, there should be a corresponding file note, meeting record, ROA, or piece of correspondence. If the OSA promised four quarterly portfolio reviews and the file shows two, that’s a disclosure problem, not a wording problem.

- Fees-charged reconciliation.Pull the platform fee reports HUB24, Netwealth, BT Panorama, CFS Edge, Macquarie Wrap, whichever applies and reconcile against the disclosure to the cent. Mid-year fee rebates thatweren’t corrected on the consent are a recurring trip-up.

- Forward-feecalculation ofevidence. If the next 12 months’ fee is a reasonable estimate, the working should be on file: assumed FUM, growth assumption, fee schedule. ASIC has flagged vague forward estimates as a surveillance finding more than once.

- Account-holder identification.Where fees are deducted from a super account, the consent must be signed by the account holder. Joint investment accounts and corporate trustees need additional sign-off care.

- Consent mechanism and audit trail.Wet signature,DocuSign, Adobe Sign, the mechanism is fine if the audit trail is intact. Confirm that the executed PDF is sitting in the CRM with an unaltered timestamp.

- Withdrawal of consentwording. The document must clearly state how the client withdraws consent and the timeframe. Generic “contact us to make changes” is not enough.

- Code of Ethics Standard 7 cross-check. Standard 7 of the Code of Ethics requires that fees and benefits are fair and reasonable and represent value for money. A paraplanner reviewing the consent should sanity-check that prior-year fees against services delivered would survive a Standard 7 question if it landed.

ASIC guidelines for fee disclosure statements: what’s still in focus

The ASIC guidelines for fee disclosure statements have been one of the most consistent enforcement themes since the Hayne Royal Commission. Across INFO 286, Report 636 (the regulator’s original FDS surveillance), and subsequent enforcement releases, the focus areas sit on three pillars:

- Accuracy. Disclosed fees match what was actually charged, to the cent. Rounding errors and platform fee rebates are not acceptable for explanations.

- Service delivery. Services described in the OSA were actually provided, and the file evidence proves it.

- Authority. Every dollar deducted from a client’s account is supported by current, valid consent, Full stop.

ASIC’s 2021 review of compliance with the new ongoing fee provisions found that around two in five files reviewed had at least one disclosure or consent shortcoming. The DBFO reforms reduce the number of moving parts, but they raise the bar on the single consent that remains. The paraplanner is now the gate, not just one of the three.

What this means for paraplanning teams

The consolidated form is shorter, but the underlying compliance work is no smaller. Practices that previously ran the FDS and consent processes on separate cycles now have one annual deadline per client, and missing it cuts off the licensee authority to deduct fees, full stop.

For internal paraplanning teams, the workflow shifts. The annual fee consent run is no longer two staggered processes; it’s a single, calendar-anchored sprint per client’s cohort. For practices that outsource paraplanning, the brief to the support partner needs to explicitly cover the consent stage, not just SOA and ROA drafting. The ongoing fee arrangements regulations Australia operates under leave very little room for “we got most of it right.”

Conclusion

The Annual Fee Consent and FDS Checklist is no longer a two-document juggle, but the consolidated form carries more weight than either predecessor did on its own. One missed anniversary, one unevidenced service, or one figure that doesn’t reconcile the platform report can knock out the licensee’s authority to charge fees for that client. For paraplanning teams like NCSGX, the win is in process discipline a repeatable checklist run on every consent turns the new regime from a compliance risk into a routine annual deliverable.

How NCSGX supports paraplanning teams with Annual Fee Consent and FDS

NCSGX’s paraplanning team handles ongoing fee consent renewals as part of the broader paraplanning support service. Typical scope across an annual consent run includes:

- Anniversary-date scheduling and 90-day pre-renewal reminders

- Drafting the consolidated consent on the practice’s licensee-approved template

- Reconciling prior-year fees against platform reports

- Building the forward-fee estimate working paper

- Cross-checking services delivered against OSA commitments

- Coordinating client communication windows with the adviser

The team also supports practices working through the broader SOA and ROA preparation workflow and licensee-level advice compliance reviews.

For a practice with 200 ongoing fee clients, the annual consent run can absorb 150–200 paraplanner hours if it’s done in-house from scratch. A structured outsourced workflow typically cuts that by half while strengthening the audit trail.

Frequently Asked Questions (FAQ)

1. Is the FDS still required after DBFO?

The standalone FDS as it existed before 10 January 2025 has been consolidated into the single annual Ongoing Fee Consent. The historical fee and service disclosures previously in the FDS now sit inside the consent document.

2. What happens if the annual consent isn't renewed on time?

The fee recipient loses the legal authority to deduct fees from the client’s account. Continuing to deduct after consent has lapsed is a contravention of the Corporations Act and triggers ASIC notification obligations for the licensee.

3. Can the consent be electronic?

Yes. ASIC accepts electronic consent provided there is a clear audit trail for a signed PDF, a DocuSign certificate, or an equivalent verifiable mechanism.

4. Do all ongoing fee clients need a consent, or only those onboarded after 10 January 2025?

All ongoing fee clients. Pre-existing arrangements transitioned onto the new regime under the DBFO for transitional provisions.

5. Who must sign the consent?

The account holder. Where fees are deducted from a super account or jointly held investment account, the relevant account holder(s) must sign.