USA

USA

Canada

Canada

Australia

Australia

Running your own super fund means you wear two hats: investor and administrator. The administrator’s hat gets heavy around lodgment time. This SMSF annual return checklist from NCSGX walks you through what to review before you lodge for the 2025–26 income year, so the audit runs smoothly, the numbers reconcile, and you’re not chasing missing paperwork the night before the deadline.

The SMSF annual return (SAR) is more than a tax return. It reports your fund’s income tax, regulatory information, and member contributions in one form to the ATO. Get the prep right, and the rest of the process is mostly a formality. Skip a step and you can end up with a late lodgment, a qualified audit, or a fund that loses its complying status.

What This SMSF Annual Return Checklist Helps You Do

Use this checklist to:

- Confirm your fund’s correct lodgment pathway and due date

- Gather clean records before handing them to your approved SMSF auditor

- Catch valuation, contribution, and pension issues before they become audit problems

- Meet your SMSF trustee obligations and keep the fund compliant

Work through it in order. Each section feeds the next, and the audit can’t start until the records below are complete.

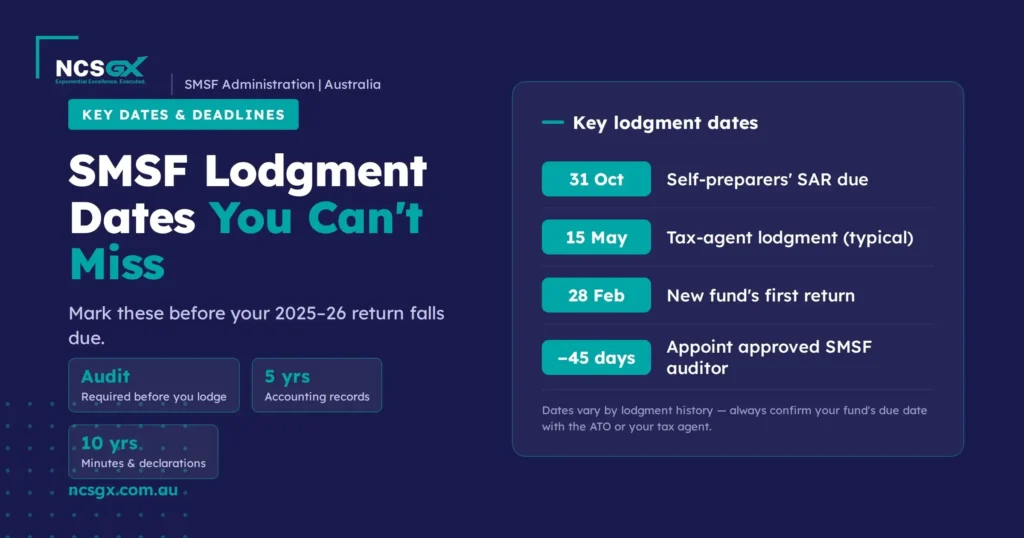

Confirm the Income Year, Lodgment Pathway and Due Date

The 2026 SMSF annual return covers the 2025–26 income year 1 July 2025 to 30 June 2026. Before anything else, confirm how your fund lodges and when it’s due, because the date depends on who prepares the return and your fund’s lodgment history.

| How the SAR is prepared | Typical due date |

| Self-preparing trustee | 31 October |

| Lodged through a registered tax agent | Usually 15 May (varies by lodgment record) |

| Newly registered SMSF (first return) | Generally 28 February when lodged via a tax agent |

These dates can shift, and the ATO sets your fund’s actual due date based on its lodgment history and compliance record. Always confirm your specific date through ATO Online services or with your tax agent before relying on it. A fund with an overdue prior-year return can have its due date brought forward.

Gather the Core SMSF Records Before the Audit

Your approved SMSF auditor can’t sign off on what they can’t see. Pull these together before the audit starts incomplete records are the single most common cause of delays.

- Bank statements for every fund account, full year

- Investment statements, contract notes, and dividend or distribution records

- Property documents, lease agreements, and rental records (if the fund holds property)

- Signed financial statements and member statements

- Trustee minutes and resolutions for the year, including the annual investment strategy review

- Contribution and rollover records for each member

- The prior-year audit report and any management letter

SMSF record-keeping requirements are specific about how long you hold these. Accounting records, annual returns, and financial statements must be kept for five years. Trustee minutes, member and trustee declarations, consents to act, and records of any change of trustee must be kept for ten years. Keep them in a form the ATO and your auditor can access.

Check Fund and Member Details Are Correct

Small data errors cause big headaches at lodgment. Before the return goes in, verify:

- The fund’s name, ABN, and TFN match ATO records

- The fund’s electronic service address (ESA) is current and active for SuperStream

- Each member’s name, date of birth, and TFN are correct

- Trustee or director details reflect any changes made during the year

- The fund’s bank account for ATO refunds and payments is recorded correctly

If you changed trustees or moved from individual trustees to a corporate trustee during the year, confirm the ATO has the update and that the trust deed and ASIC records align.

Review Asset Valuations at Market Value

This is where many trustees come unstuck. Under the super rules, you must value the fund’s assets at market value for the financial accounts and statements every year not at cost, and not at a number that feels about right.

For listed shares and managed funds, market value is straightforward from year-end statements. For property, collectables, unlisted shares, or units in private trusts, you need objective and supportable evidence. That might be a recent independent valuation, comparable sales, a rates notice combined with market data, or net asset backing from audited accounts. Keep the evidence on file, your auditor will ask for it, and “we estimated it” won’t pass.

If the fund holds harder-to-value assets, sort the valuation evidence early. It’s the item most likely to hold up an audit.

Review Contributions, Rollovers and Member Balances

Reconcile every dollar that went in and out for each member, then check it against the caps for 2025–26:

- Concessional (before-tax) contributions: $30,000 per member

- Non-concessional (after-tax) contributions: $120,000 per member, or up to $360,000 under the three-year bring-forward, subject to the member’s total super balance

Confirm employer contributions were received and allocated to the right member, that any rollovers in or out were processed through SuperStream, and that no member has unintentionally breached a cap. Where a member is near a threshold, flag it now rather than after lodgment. These caps apply to the 2025–26 year confirm current figures with the ATO before you rely on them, as they’re indexed periodically.

Check Pension Payments and Retirement-Phase Details

If a member is in pension phase, the fund must have paid the minimum pension for the year based on the member’s age and account balance at 1 July 2025. Falling short, even by a small amount, can mean the pension is treated as having stopped, with tax consequences on the fund’s earnings.

Also confirm:

- Pension payments are documented and were actually paid from the fund (not just journalled)

- Any new pension was reported through the transfer balance account report (TBAR)

- No member has exceeded the transfer balance cap of $2.0 million (from 1 July 2025)

Run a Practical SMSF Compliance Check Before Lodgment

A quick SMSF audit checklist trustees can run before handing over the file:

- Sole purpose of the test is to determine whether the fund exists to provide retirement benefits, nothing else

- No loans or financial assistance to members or relatives

- In-house assets within the 5% limit

- Related-party transactions on arm’s-length terms

- Investment strategy reviewed and documented, with insurance considered for members

- Assets held in the fund’s name and clearly separated from personal assets

If any of these raise a flag, deal with it before lodgment. A breach you’ve identified and corrected is a far better position than one your auditor finds for you.

Complete the Final Pre-Lodgment Review

Before you press submit:

- Financial statements are signed by trustees

- The audit is complete and you hold the audit report remember, the audit must be done before you lodge

- The SAR figures match the audited financial statements

- The supervisory levy and any tax payable are accounted for

- Member contribution amounts in the SAR match your reconciliations

The auditor must be an approved SMSF auditor registered with ASIC, must be independent of the fund, and must be appointed at least 45 days before the SAR is due. Leave the appointment too late and you risk missing your lodgment date.

What Trustees Should Do After Lodgment

Lodgment isn’t the finish line. Once the SAR is in:

- Pay any tax and the SMSF supervisory levy by the due date

- File the audit report, financial statements, and minutes for the record (remember the 5- and 10-year retention periods)

- Action any issues raised in the auditor’s management letter

- Diarise next year’s key dates auditor appointment, valuation evidence, and the investment strategy review

A clean year-end makes next year’s far easier. The funds that lodge without drama are the ones that keep tidy records all year, not the ones that scramble in October.

Conclusion

The SMSF annual return rewards trustees who prepare. Confirm your due date, gather complete records, value assets properly, reconcile contributions and pensions, and appoint your approved SMSF auditor early. Work through this checklist before lodgment and you protect the fund’s complying status and your own peace of mind.

If the administration is becoming a year-round burden, that’s usually a sign it’s time to get specialist support behind your fund.

How NCSGX Can Help

NCSGX Australia provides outsourced SMSF administration and back-office support that takes the year-round compliance load off accounting firms and trustees. We prepare audit-ready files, reconcile contributions and pensions, organise valuation evidence, and keep records in order so lodgment is clean and on time.

We administer; we never advise your accountant and auditor keep their roles, and we make their job (and yours) easier. To talk through how we support SMSF administration, get in touch with the NCSGX team.

Frequently Asked Questions (FAQ)

1. Does an SMSF need an audit before lodging the annual return?

Yes. Every SMSF must be audited by an approved SMSF auditor each year before the annual return is lodged, regardless of whether the fund has tax to pay or has been active. The audit report must be complete first.

2. What records are needed for an annual SMSF return?

Bank and investment statements, contract notes, dividend and distribution records, property and lease documents, signed financial and member statements, trustee minutes, contribution and rollover records, and the prior-year audit report. Accounting records are kept for five years; minutes and declarations for ten.

3. Who is responsible for SMSF lodgment?

The trustees. Even if you use an accountant, administrator, or tax agent to prepare and lodge, the legal responsibility for an accurate, on-time return sits with the trustees of the fund.

4. How are SMSF assets valued for the annual return?

At market value, every year, supported by objective and supportable evidence. Listed assets use year-end statements; property, collectables, and unlisted assets need independent valuations or comparable market evidence kept on file for the auditor.

5. What happens if an SMSF annual return is late?

A late SAR can trigger ATO penalties and, importantly, can cause the fund to be listed as having a “regulation details removed” status on Super Fund Lookup which can stop employers and other funds from making contributions or rollovers to it.

6. Do pension-phase SMSFs still lodge an annual return?

Yes. A fund in pension phase still lodges an annual return each year, must still be audited, and must still meet its minimum pension payment and reporting obligations.