USA

USA

Canada

Canada

Australia

Australia

Every self-managed super fund in Australia needs a written SMSF investment strategy, and it’s not just paperwork to keep your auditor happy. It’s the document that proves you’re running the fund deliberately, not just buying assets as the mood takes you. Get it right and your annual audit is smoother, your decisions are easier to justify, and your members’ retirement money is working toward a clear goal.

This guide walks through what the strategy has to cover in 2026, shows you a few worked examples, and gives you a structure you can adapt to your own fund. If the admin side of all this is eating your weekends, NCSGX handles SMSF administration and back-office work for accounting firms and trustees across Australia.

What is an SMSF investment strategy?

An SMSF investment strategy is a written plan that sets out how your fund will invest its money to meet the members’ retirement goals. It covers what you’ll invest in, in what proportions, why those choices suit your members, and how you’ll manage risk and liquidity along the way.

It is not a stock-picking document. The ATO isn’t asking which shares you’ll buy on Tuesday. It wants evidence that the trustees have thought about the fund’s objectives and built a plan that fits them. The strategy is reasoning; the investments are how you act on it.

Is an investment strategy for SMSF trustees a legal requirement?

Yes. Preparing and maintaining an investment strategy for SMSF trustees is a legal obligation under regulation 4.09 of the Superannuation Industry (Supervision) Regulations 1994. Trustees must formulate, regularly review, and give effect to a written strategy that has regard to the whole circumstances of the fund.

Skip it, run an out-of-date one, or hold a strategy that doesn’t match what the fund owns, and you’re looking at a contravention your auditor must report. The ATO can apply penalties, and in serious cases the fund can lose its complying status. This is the single most common compliance issue auditors’ flag, so it’s worth doing properly the first time.

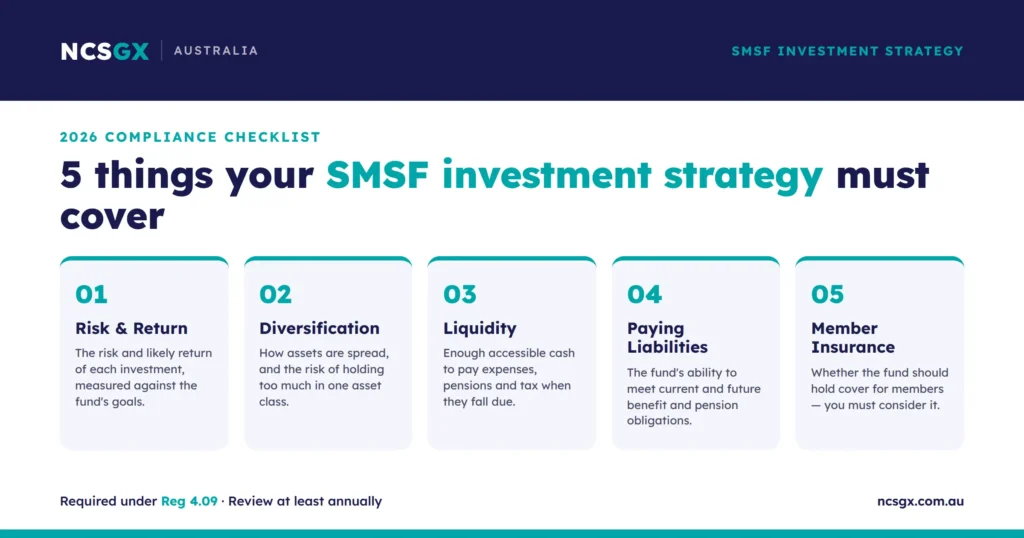

What must your self-managed super fund investment strategy cover?

A compliant self-managed super fund investment strategy sits within the broader SMSF investment requirements trustees must meet, and has to address five specific factors set out in the regulations. Each one needs genuine consideration, documented in writing.

| Factor | What you need to address |

|---|---|

| Risk and return | The risk of making, holding and selling each investment, and the likely return, measured against the fund’s objectives and cash flow needs. |

| Diversification | How the fund’s assets are spread, and the risk of holding too much in one asset, asset class, or location. |

| Liquidity | Whether the fund holds enough accessible cash to pay expenses, pensions, and tax when they fall due. |

| Ability to pay liabilities | Whether the fund can meet current and future obligations, such as benefit payments and minimum pension drawdowns. |

| Insurance for members | Whether the fund should hold life, TPD, or income protection cover for its members (you must consider it, even if you decide against it). |

That last point trips up a lot of trustees. You don’t have to take out insurance, but you do have to show you thought about whether the fund should. A single line confirming the decision is enough to satisfy the requirements.

SMSF investment strategy examples

The right asset mix depends entirely on your members’ age, risk appetite, and how close they are to retirement. The SMSF investment strategy examples below show how that plays out across three common profiles. These are illustrations, not advice, but they give you a feel for how the ranges shift.

| Profile | Cash & fixed interest | Australian & global shares | Property | Other (alts) |

|---|---|---|---|---|

| Growth (members in their 30s–40s) | 5–15% | 60–80% | 10–25% | 0–10% |

| Balanced (members in their 50s) | 15–30% | 40–60% | 15–35% | 0–10% |

| Conservative / pension phase | 30–50% | 20–40% | 10–30% | 0–5% |

Notice the range. The ATO doesn’t want a strategy that simply allows “0–100%” in every asset class, because that says nothing about your actual intentions. Set ranges that genuinely reflect how the fund is run and update them when the plan changes.

How to write your SMSF investment strategy step by step

You can draft a sound strategy in an afternoon if you work through it in order:

- Set the fund’s objective. Be specific. “Grow the fund to support a comfortable retirement from 2040 with moderate risk” beats “make good returns.”

- Profile your members. Their ages, balances, contribution patterns, and how soon they’ll need to draw an income to shape everything else.

- Decide your asset allocation. Set target ranges across cash, shares, property, and any alternatives, and write down why each range suits the fund.

- Address all five factors. Risk, return, diversification, liquidity, ability to pay liabilities, and insurance, each with a sentence or two of reasoning.

- Set a review trigger. Note that you’ll review at least annually and whenever a major event occurs.

- Sign and date it. All trustees (or directors of the corporate trustee) should sign, and you keep it with your fund’s records.

Best SMSF strategies the ATO expects to see

When people search for the best SMSF strategies, ATO auditors will accept. What they’re really asking is how to avoid getting flagged. A few habits separate a strategy that passes cleanly from one that draws questions:

- Tailor it to your fund. Generic templates with boilerplate ranges are the fastest way to attract scrutiny. The strategy should read like it was written for your members.

- Justify concentration. If the fund holds 90% or more in a single asset, such as one property bought through a limited recourse borrowing arrangement, document why that lack of diversification is appropriate. The ATO has written directly to thousands of trustees about this.

- Keep cash for drawdowns. A pension-phase fund holding only illiquid property can’t meet its minimum pension payments. That’s a liquidity failure, and it’s avoidable.

- Match the document to reality. If your strategy says 60% shares and the fund actually holds 90% property, the strategy is meaningless. Update it when your holdings move.

How often should you review your SMSF investment strategy?

At least once a year, and the ATO expects you to record that the review happened even if nothing changes. For many practices, this review sits naturally alongside broader EOFY preparation and client file clean-up. Beyond the annual check, review the strategy whenever something material shifts:

- A member joins, leaves, or starts a pension

- A large contribution or rollover lands

- The fund makes a significant purchase or sale

- Markets move sharply enough to push your allocation outside its target ranges

- A change in the law affects how the fund should be run

A short, dated file note confirming the review is enough. The point is to show the strategy is a living document, not something signed once and forgotten.

Common SMSF investment strategy mistakes to avoid

- Copy-paste templates that don’t reflect the fund’s real members or holdings

- “0–100%” ranges across every asset class, which signal no real decision was made

- Never reviewing it after the first year

- Ignoring liquidity in a pension-phase fund that can’t fund its drawdowns

- Forgetting the insurance consideration entirely

- Letting the document drift out of step with what the fund owns

Conclusion

A strong SMSF investment strategy does two jobs at once: it keeps you compliant under regulation 4.09, and it forces the kind of clear thinking that actually protects your members’ retirement savings. Set a real objective, choose asset ranges that fit your members, address the five required factors, and review them every year. Do that, and the strategy stops being a chore and starts being the backbone of how you run the fund.

If reviewing strategies, reconciling assets, and preparing audit-ready files for a growing book of SMSFs is stretching your team, that’s exactly the work NCSGX’s outsourced SMSF administration takes off your plate.

Ready to free up your team this SMSF season? Connect with the NCSGX team to talk through your fund volumes, turnaround times, and where outsourcing fits.

How NCSGX can help

NCSGX provides outsourced SMSF administration, accounting, and superannuation compliance support to Australian accounting firms and trustees. Our team prepares and reviews investment strategies, reconciles fund assets, manages member statements, and produces audit-ready financials so your fund stays compliant, and your in-house team stays focused on advice and client relationships.

If you run an accounting or advice practice, our accounting and compliance support scales with your SMSF book without you having to hire and train through every busy season. To talk through your fund volumes and turnaround needs, get in touch with the NCSGX team.

Frequently asked questions (FAQ)

1. Does every SMSF need a written investment strategy?

Yes. It’s required under regulation 4.09 of the SIS Regulations, regardless of the fund’s size or how many members it has.

2. Can I use a free SMSF investment strategy template?

A template is a fine starting point, but it must be customised to your fund’s members, objectives, and actual asset mix. A generic, unedited template is one of the most common reasons auditors raise a flag.

3. How often do I need to review my SMSF investment strategy?

At least annually, plus whenever a significant event occurs, such as a member starting a pension, a large contribution, or a major change in the fund’s investments.

4.What happens if my SMSF doesn't have a compliant strategy?

Your auditor must report it to the ATO. Depending on the severity, the ATO can apply administrative penalties and, in serious cases, treat the fund as non-complying, which carries significant tax consequences

5. Do I have to take out insurance for members?

No, but you do have to consider whether the fund should hold insurance and document that decision either way.