USA

USA

Canada

Canada

Australia

Australia

T2 Corporate Tax Return in 2026: Step-by-Step Guide on Filing

The T2 corporate tax return is one of the most consequential compliance obligations a Canadian corporation faces each fiscal year. Whether you lead a mid-market manufacturing firm or a professional services company with multiple shareholders, the stakes of getting this filing right are significant.

Late submissions, miscalculated tax payable, or improperly claimed deductions can trigger CRA audits, interest charges, and penalties that compound quickly.

For CFOs and senior finance executives, this guide cuts through the noise and delivers a precise, actionable overview of what the T2 return requires, how to approach filing in 2026, and where most corporations quietly leave money on the table.

What Is a T2 Corporate Tax Return in Canada?

The T2 corporation income tax return is the mandatory annual filing that every corporation incorporated in Canada must submit to the Canada Revenue Agency (CRA). It reports the corporation’s income, deductions, credits, and taxes payable for a given fiscal year. Unlike individual income tax returns, the T2 is required regardless of whether the corporation earned any income during the year or is claiming a loss.

The CRA uses the T2 to assess federal and, in most provinces, provincial corporate income tax. The form is comprehensive, often accompanied by multiple supporting schedules that detail everything from capital cost allowance claims to related-party transactions.

For a deeper understanding of the CRA’s requirements, visit the Canada Revenue Agency’s official T2 corporate tax return page.

Who Needs to File a T2 Corporate Tax Return?

Any corporation that was resident in Canada at any point during a fiscal year is required to file a T2 return for that year. This covers a broad range of entities, including:

- Canadian-controlled private corporations (CCPCs) eligible for the small business deduction

- Public corporations listed on Canadian exchanges

- Non-resident corporations that carried on business in Canada or disposed of taxable Canadian property

- Inactive or dormant corporations that remain incorporated but have no activity

The obligation does not disappear simply because a company had zero revenue. A corporation must file as long as it remains legally incorporated. Failure to do so can result in director liability, loss of good standing with the CRA, and complications during due diligence for future financing or acquisition transactions.

According to CRA data, there are over 2.9 million active business corporations in Canada, and corporate tax compliance is one of the agency’s primary enforcement priorities. Ensuring your corporation is among those in good standing is a baseline requirement, not an optional goal.

Step-by-Step Guide to Filing a T2 Corporate Tax Return in 2026

Understanding how to file a T2 return properly requires more than downloading a form. The process demands precision, complete records, and an understanding of applicable deductions and credits. Here is a structured approach for 2026.

Step 1: Gather and Finalize Financial Records

Before completing any CRA form, your corporation’s financial statements must be accurate and reconciled. This includes your income statement, balance sheet, and notes to the financial statements. Ensure your general ledger is closed for the fiscal year and that all accruals, adjustments, and intercompany transactions are reflected correctly.

For corporations with revenues exceeding $1 million or those subject to audit risk, having financial statements prepared or reviewed by a licensed CPA is strongly advisable before beginning the tax filing process.

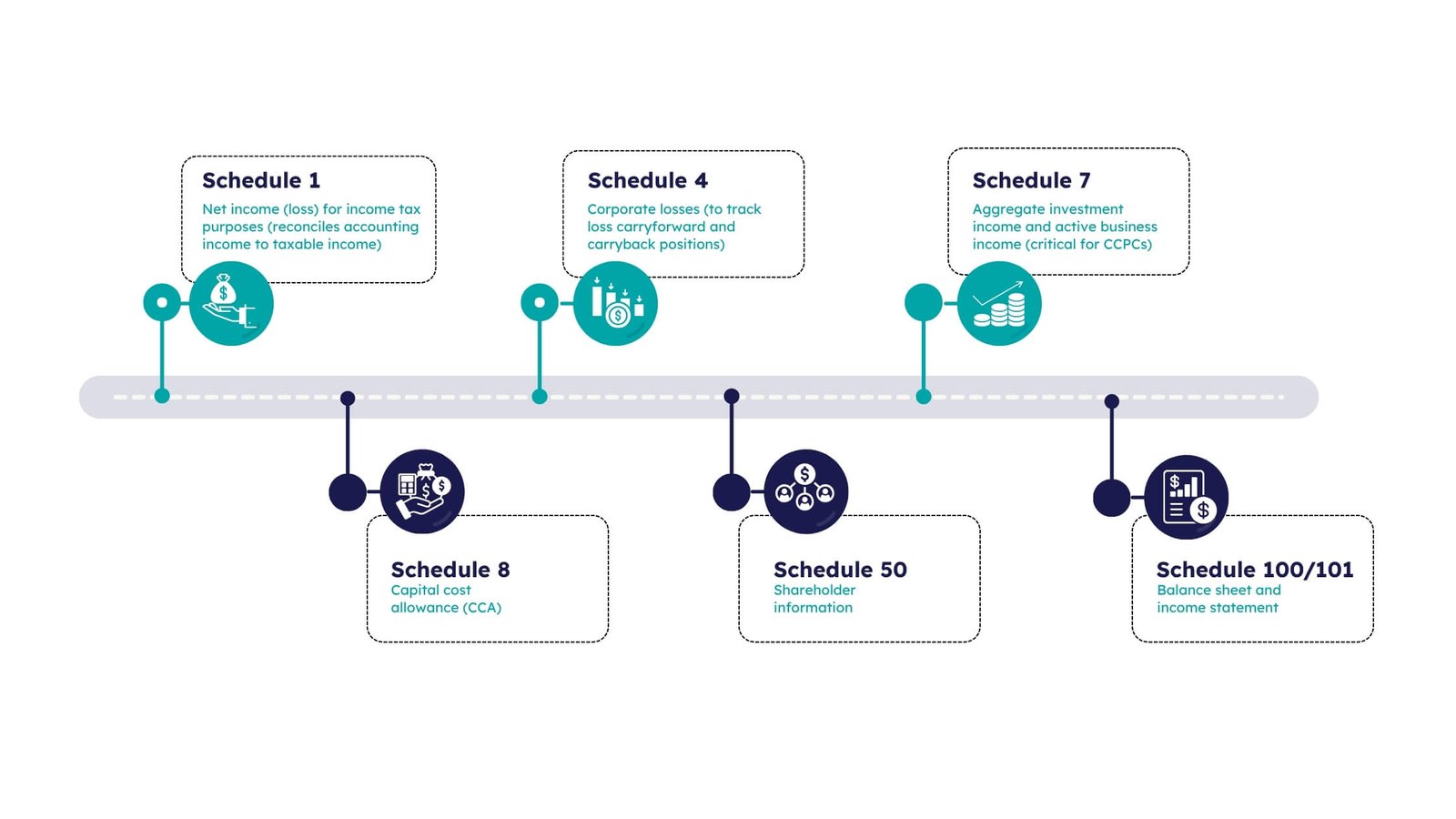

Step 2: Complete the T2 Return and Required Schedules

The T2 return is a multi-page document. Most corporations will also need to complete several schedules that support the core return:

The specific schedules required will depend on your corporation’s activities, industry, and structure. Missing a required schedule is a common error that can trigger a CRA review.

Step 3: Calculate Taxes Payable

Once income is determined, the applicable federal and provincial tax rates must be applied. For CCPCs in 2026, the federal small business deduction rate applies on the first $500,000 of active business income, with the general corporate rate applying above that threshold.

Additional considerations at this stage include:

- Provincial tax credits that vary by province

- Scientific Research and Experimental Development (SR&ED) credits for qualifying R&D expenditures

- Manufacturing and processing deductions

- Eligible Capital Expenditures under relevant CCA classes

- Foreign tax credits for corporations with international operations

This is also where the distinction between tax payable and instalments becomes critical. If your corporation made quarterly tax instalments throughout the year, those payments are applied against your year-end balance owing.

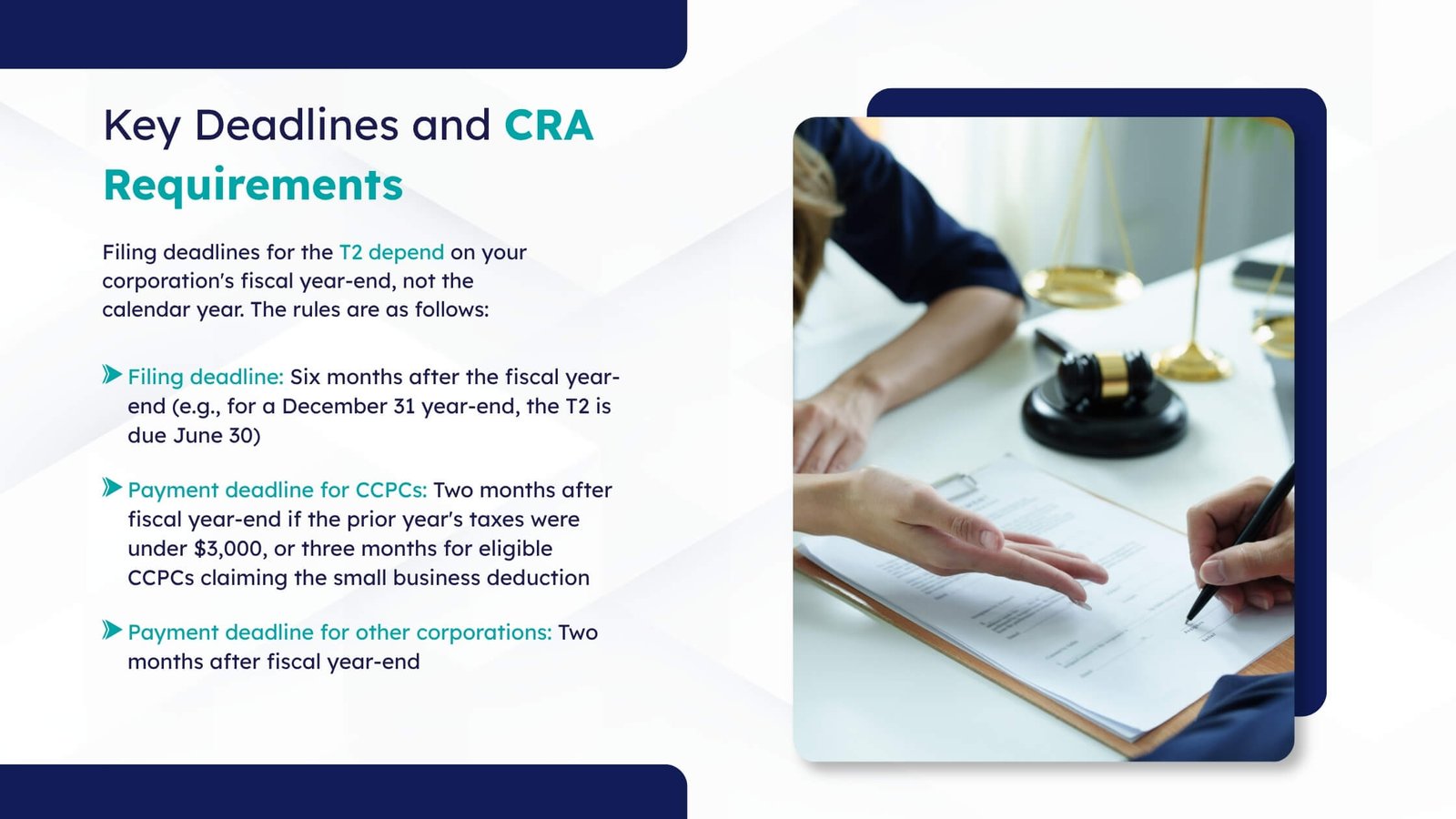

Step 4: Submit to the CRA

The T2 must be filed electronically using CRA-certified software if the corporation has gross revenues over $1 million. Smaller corporations may file in paper format, though electronic filing is increasingly standard across all sizes.

Most tax professionals use CRA-certified software such as TaxCycle, Cantax, or Profile to file corporate tax return electronically. A confirmation number issued by the CRA upon receipt serves as proof of submission.

For a practical resource on filing options and software tools, TurboTax Canada’s corporate tax filing guide is a useful reference point for smaller corporations navigating the process independently.

The distinction between the filing deadline and the payment deadline is one that regularly catches corporations off guard. You may have until June to file but be required to pay any balance owing by the end of February or March. Interest on unpaid balances begins accruing the day after the payment deadline, at the CRA’s prescribed rate.

Failure to file on time results in a late-filing penalty equal to 5% of the balance owing, plus 1% per additional month, up to a maximum of 12 months. Repeat offences carry higher penalties.

Common Mistakes in Corporate Income Tax Filing

Even experienced finance teams make filing errors that cost time, money, and CRA goodwill. The most recurring issues we see in corporate income tax filing include:

- Missing or incorrect schedules: Filing a T2 without all required supporting schedules is an incomplete return. The CRA will request the missing information, delaying your assessment.

- Improper CCA claims: Claiming capital cost allowance on assets that do not qualify, or using the wrong CCA class, leads to adjustments and potential penalties.

- Shareholder loan misclassification: Loans to shareholders must be repaid within one year of the fiscal year-end in which they arose, or they become a taxable benefit. This is one of the most litigated areas in private corporation tax.

- Underreporting inter-company transactions: Transfer pricing rules apply even to domestic related-party transactions in some cases. Inadequate documentation creates audit exposure.

- Missed tax credits: SR&ED credits, provincial investment tax credits, and hiring incentives are frequently unclaimed by corporations that do not have a dedicated tax function reviewing eligibility annually.

Why Businesses Outsource T2 Tax Return Preparation

For many corporations, the real question is not whether they can handle corporate income tax filing internally, but whether they should. As regulatory complexity increases and CRA audit activity intensifies, the cost-benefit analysis is shifting in favour of outsourcing.

The core arguments for outsourcing T2 preparation include:

- Access to specialized tax expertise that keeps pace with annual legislative changes, new CRA interpretive bulletins, and evolving case law

- Reduced risk of costly errors that trigger interest, penalties, or audits

- Efficient use of internal finance resources who can focus on financial planning and analysis rather than compliance mechanics

- Proactive tax planning that integrates corporate structure, remuneration planning, and investment decisions with annual filing obligations

Outsourcing does not mean surrendering control. The best providers operate as an extension of your team, delivering transparent reporting, clear documentation, and consistent communication throughout the filing cycle.

Ready to simplify your corporate tax obligations? Explore NCSGX Canada’s tax services.

How NCSGX Canada Supports Your Corporate Tax Filing

At NCSGX Canada, our corporate tax practice is built specifically to serve the needs of growth-stage and established businesses across Canada. We work with corporations across a range of industries, from technology and real estate to professional services and manufacturing, and we understand that no two T2 returns are the same.

Our approach to T2 tax return preparation includes:

We do not treat the T2 as a compliance checkbox. We treat it as a planning document. Every filing is an opportunity to assess your corporation’s tax position, review remuneration strategies, and position the business for the year ahead.

For executives who want a filing partner that brings both technical depth and business judgment to the table, NCSGX Canada is the clear choice. Contact us to schedule your corporate tax consultation and let our team handle the complexity while you focus on leading your business.