USA

USA

Canada

Canada

Australia

Australia

The OAS clawback 2026 is one of the most consequential retirement income rules a Canadian senior can face. Formally known as the Old Age Security recovery tax, it requires higher-income retirees to repay a portion of their OAS pension when net income exceeds a government-set threshold. For the 2026 tax year, that threshold sits at $95,323, a figure indexed annually to inflation.

The OAS clawback 2026 is one of the most consequential retirement income rules a Canadian senior can face. Formally known as the Old Age Security recovery tax, it requires higher-income retirees to repay a portion of their OAS pension when net income exceeds a government-set threshold. For the 2026 tax year, that threshold sits at $95,323, a figure indexed annually to inflation.

Many retirees assume the clawback only affects the very wealthy. That assumption is increasingly costly. A single RRIF withdrawal, a capital gain from selling an investment property, or even continued part-time employment can push a retiree across the line without any warning.

The OAS clawback 2026 Canada seniors face today is broader in reach than most people expect, and it is catching more retirees each year simply due to rising CPP amounts and pension income.

Understanding how the Canada OAS clawback 2026 rules apply to your specific income situation is worth doing well before the numbers are set. This guide explains how it works, what has changed, and how to plan around it effectively with NCSGX.

What is OAS Clawback 2026?

The OAS clawback is a mechanism through which the Canada Revenue Agency (CRA) gradually recovers Old Age Security payments from retirees whose net world income exceeds a defined threshold.

The program is designed to concentrate OAS benefits among seniors with limited retirement resources, while phasing out payments to those who, in the government’s view, have sufficient income from other sources.

Officially called the OAS recovery tax, it is not a separate bill that arrives in the mail. Instead, the CRA automatically reduces monthly OAS payments in advance based on the income you reported on your previous year’s tax return. If the final clawback amount differs from what was withheld, the difference is reconciled when you file your tax return.

The 2026 OAS clawback continues to operate on the same structural basis as prior years, but updated income thresholds, modest inflationary adjustments, and an expanded senior population make it worth examining with fresh eyes. The program draws its authority from the Old Age Security Act, and all recovery tax calculations are administered by the CRA.

Key Points: How the Clawback Is Applied

- It reduces your monthly OAS pension directly, not as a separate tax assessment.

- It applies only to individual income, not household or combined spousal income.

- The CRA uses net world income from line 23600 of your tax return. Similar income-based assessments are also used for several federal benefit programs, including the GST/HST credit payment system in Canada.

- OAS receipt begins at age 65 but can be deferred to age 70 for a permanent monthly increase.

OAS Clawback Threshold 2026

Because the OAS program runs on a July-to-June cycle rather than a calendar year, there are effectively two different sets of thresholds that matter in 2026, depending on which period you are reviewing. Additionally, the CRA applies a third set of figures for income earned during the 2026 calendar year, which will affect OAS payments from July 2027 onward.

The table below outlines the minimum recovery thresholds (where clawback begins) and the maximum recovery thresholds (where OAS is fully eliminated) for each applicable period. Seniors aged 75 and over face a slightly higher maximum threshold because their base OAS amount was permanently increased by 10% beginning in July 2022.

*2026 income year figures are based on projected inflation indexing and the CRA’s established adjustment methodology. Confirm final figures on your 2026 Notice of Assessment or via the CRA website at canada.ca.

The recovery rate across all periods remains consistent: for every dollar your net income exceeds the minimum threshold, 15 cents of OAS is recovered. This rate has not changed. What changes year over year is where the threshold is set.

How the OAS Clawback Works in Canada

The mechanics are straightforward, though their impact is easy to underestimate. The CRA calculates your OAS clawback using the following formula:

Clawback Amount = (Net World Income – Minimum Threshold) x 15%

Step one is determining your net world income, which is the figure reported on line 23600 of your federal tax return. This includes all sources of taxable income: CPP, private pensions, RRIF and RRSP withdrawals, employment income, rental income, taxable capital gains, and investment income. It does not include TFSA withdrawals, which are tax-free and therefore invisible to the CRA for clawback purposes.

Step two is comparing that figure to the minimum threshold for the relevant income year. If your income is below the threshold, no clawback applies. If it is above, the CRA applies the 15% recovery rate to the excess.

Step three is the timing adjustment. Because the OAS program year runs from July to June, the clawback recovery is applied prospectively. If your 2025 income exceeds $93,454, the CRA will begin deducting recovery tax from your July 2026 OAS payments through June 2027. This lag is important: financial decisions made in 2025 directly affect cash flow in 2026.

Need help calculating your net world income and clawback exposure? Our Income Tax Services team can walk you through it.

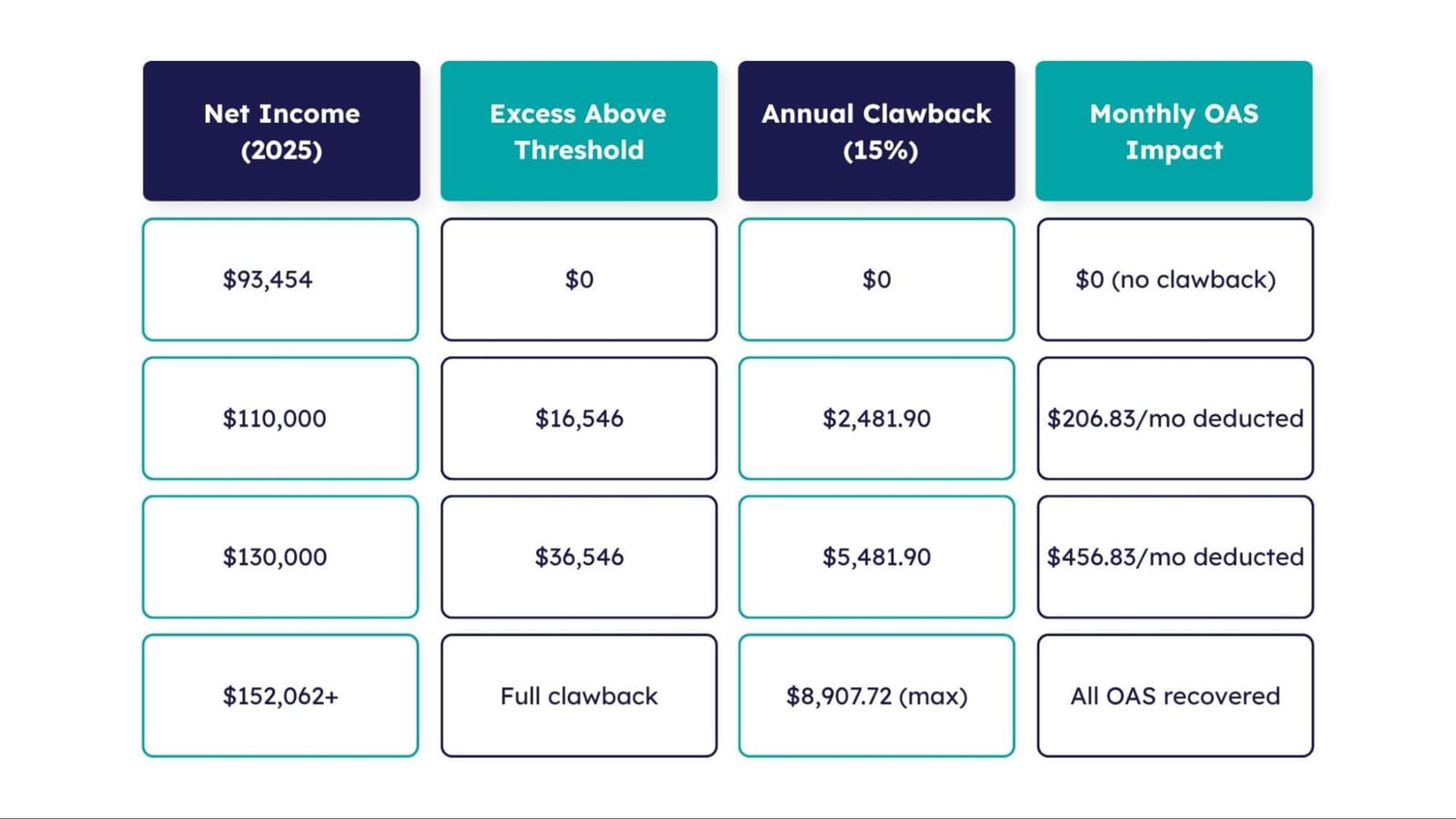

How Much OAS Can Be Reduced in 2026?

The following examples illustrate how income level translates to actual clawback exposure for the July 2026 to June 2027 OAS period. These scenarios apply to a senior aged 65 to 74, using the minimum threshold of $93,454 for the 2025 income year.

| Net Income (2025) | Excess Above Threshold | Annual Clawback (15%) | Monthly OAS Impact |

|---|---|---|---|

| $93,454 | $0 | $0 | $0 (no clawback) |

| $110,000 | $16,546 | $2,481.90 | $206.83/mo deducted |

| $130,000 | $36,546 | $5,481.90 | $456.83/mo deducted |

| $152,062+ | Full clawback | $8,907.72 (max) | All OAS recovered |

As the table makes clear, even a modest income overage can carry a meaningful monthly penalty. A retiree earning $110,000 in 2025 will see roughly $207 deducted from each OAS payment for an entire year. At $130,000, that grows to over $450 per month. These are not trivial sums, particularly for seniors on fixed incomes who depend on OAS as a predictable cash flow source.

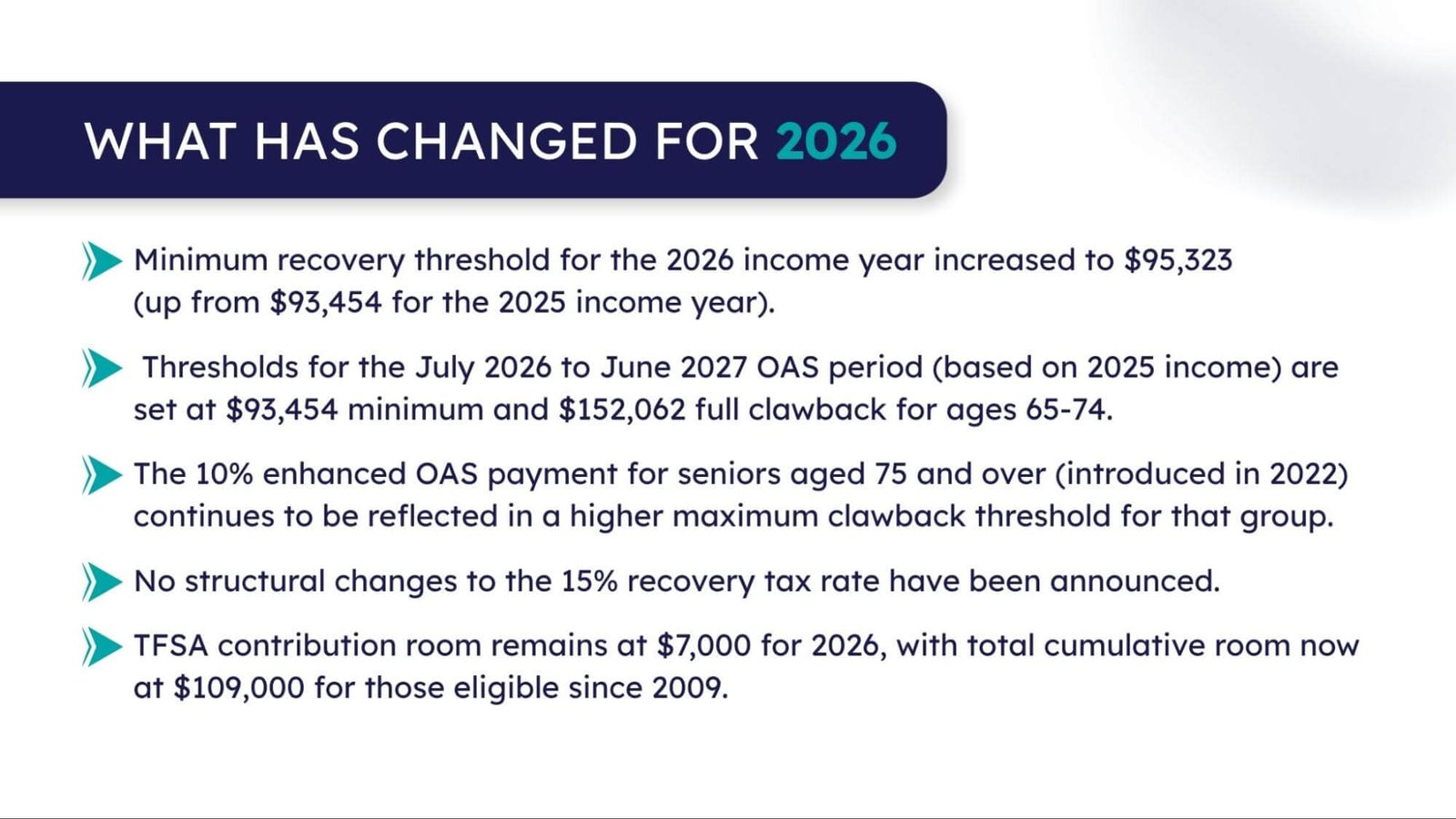

Key Changes to OAS Clawback in 2026

The 2026 OAS clawback thresholds reflect the federal government’s annual inflation-indexing process, which applies a cost-of-living adjustment to most tax parameters, including the OAS recovery thresholds. For 2026, the CRA applied a 2% indexation factor, consistent with moderating inflation relative to the elevated rates seen in 2022 and 2023.

This inflationary adjustment produced a minimum threshold of $95,323 for the 2026 income year, up from approximately $93,454 in the 2025 income year. While this is a modest increase, it does give some seniors additional room before clawback begins. The maximum full clawback thresholds have risen proportionately.

There are no announced legislative changes to the OAS recovery tax framework for 2026. The federal government has not introduced new income brackets or age-adjusted clawback rates beyond those already in effect for seniors 75 and over.

However, ongoing inflation and rising CPP and pension amounts mean a growing number of retirees are being drawn into clawback territory each year simply through ordinary income growth.

Strategies to Minimise OAS Clawback

The 2026 OAS clawback is not inevitable. With the right income structure in place, many retirees can reduce or eliminate their exposure entirely. Here are the most effective strategies:

Pension Income Splitting

- Split up to 50% of the eligible pension income with a lower-income spouse

- Reduces your individual net income, potentially below the clawback threshold

- Applies to defined benefit pensions, RRIF withdrawals (age 65+), and RRSP annuities

TFSA Maximisation

- TFSA withdrawals are completely invisible to the CRA for clawback purposes

- Draw from your TFSA before touching registered accounts wherever possible

- The cumulative TFSA room in 2026 is $109,000 per eligible individual

RRIF Withdrawal Sequencing

- Avoid large, lump-sum RRIF withdrawals in a single tax year

- Spread withdrawals steadily across multiple years to keep income stable

- Begin modest drawdowns before CPP and OAS stack on top of each other

OAS Deferral (Up to Age 70)

- Each month of deferral adds 0.6% to your monthly OAS permanently

- Deferring five full years means a 36% higher benefit for life

- A smart option if your income in early retirement would trigger clawback anyway

Capital Gains Timing

- Taxable gains count toward net world income and can spike your clawback unexpectedly

- Where possible, spread asset sales across two or more tax years

- Especially relevant for non-registered investments and investment real estate

How to Plan Your Retirement Income Around OAS Clawback

Think of the clawback threshold as a planning ceiling, not just a tax line. Here is how to build your retirement income around it:

Start Planning 3 to 5 Years Early

- You need time to restructure registered accounts, rebalance TFSAs, and sequence withdrawals properly

- Waiting until OAS begins leaves very little room to maneuver

Ask the Right Questions First

- Which of your income sources are flexible and controllable year to year?

- What is the right order to draw down your accounts to stay below $93,454 or $95,323?

- Can you reduce RRSP balances now, before CPP and OAS push your income higher?

For Couples: Equalise Income Between Partners

- The clawback is assessed individually, not as a household

- One partner earning $130,000 and another earning $40,000 creates far more clawback exposure than two partners each earning $85,000

- Pension splitting, spousal RRSPs, and TFSA rebalancing can dramatically shift the picture

Focus on the Right Income, Not Just the Highest Return

- Generating an extra percentage point of investment yield rarely matters if it pushes you across the threshold

- Staying below the minimum recovery limit is often worth more than chasing additional income

For official threshold figures and recovery tax details, visit the Government of Canada’s OAS recovery tax page.

Conclusion

The OAS clawback 2026 is not something to figure out after the fact. With thresholds now set at $93,454 for the July 2026 payment period and $95,323 for the 2026 income year, more Canadian retirees than ever are at risk of losing a portion of a benefit they have earned. The good news is that with the right income planning strategy in place, much of that exposure is avoidable.

Whether you are approaching OAS eligibility or already receiving payments, now is the right time to review your retirement income structure. Connect with the NCSGX team today and make sure your OAS benefit stays where it belongs.

body {

font-family: Arial, sans-serif;

line-height: 1.6;

margin: 20px;

color: #333;

}

h2, h3 {

color: #1f3c88;

}

b {

font-weight: 600;

}

a {

color: #1f3c88;

text-decoration: none;

}

a:hover {

text-decoration: underline;

}

ul {

padding-left: 20px;

margin-bottom: 20px;

}

table {

width: 100%;

border-collapse: collapse;

margin: 20px 0;

font-size: 15px;

}

table thead {

background-color: #1f3c88;

color: #ffffff;

}

table thead th {

padding: 12px;

text-align: left;

font-weight: 600;

}

table tbody td {

padding: 12px;

border-bottom: 1px solid #ddd;

}

table tbody tr:nth-child(even) {

background-color: #f7f9fc;

}

table tbody tr:hover {

background-color: #eef3ff;

transition: 0.3s;

}

table td, table th {

border: 1px solid #e0e0e0;

}