USA

USA

Canada

Canada

Australia

Australia

Most Canadian founders launch a business with a clear product vision and a vague bookkeeping plan. That gap shows up later, usually at the worst time: a missed GST/HST filing, a surprise CRA review, or a financing application that stalls because the books cannot back up the numbers. Strong small business bookkeeping services close that gap before it becomes expensive.

NCSGX Canada’s guide walks through what bookkeeping resilience looks like for Canadian SMEs in 2026. Where most companies trip up, which signals a call for action, and how owners, CFOs, and controllers can build a finance function that holds up when the market gets noisy.

Why Do Canadian Small Businesses Struggle with Bookkeeping?

Three forces tend to collide. Owners wear too many hats; the regulatory environment keeps shifting, and the cost of hiring a senior in-house finance lead climbs every year. The Business Development Bank of Canada (BDC) has flagged liquidity pressure and weak cash flow visibility as among the top concerns for SME owners heading into 2026, and Statistics Canada data continues to show that roughly half of Canadian small businesses close within ten years of opening, with financial mismanagement among the leading drivers.

Bookkeeping for small businesses is rarely the cause of failure on its own. It is usually the canary. When the books fall behind, decision quality follows shortly after.

Common bookkeeping challenges for Canadian SMEs

- Owners reconciling accounts only at year end, then scrambling through tax season

- Mixed personal and business banking activity inside a single account

- GST/HST input tax credits left on the table

- Payroll deductions (CPP, EI, income tax) calculated manually in spreadsheets

- Contractor vs. employee classification handled by guesswork rather than CRA criteria

- No clear chart of accounts, so reporting tells a different story every quarter

Owners new to Canada bookkeeping rules also tend to underestimate provincial sales tax complexity, particularly the PST in BC, Saskatchewan, and Manitoba, and the QST regime administered by Revenue Québec.

Key Takeaways

- Bookkeeping is a leadership issue, not just an accounting one.

- Most failures are structural – weak systems, not weak bookkeepers.

- Small mistakes compound fast: missed ITCs, late reconciliations, contractor misclassification.

- Monthly closes beat year-end scrambles.

- Visibility drives resilience – current books, current filings, fast reporting.

- Watch the warning signs – slow P&Ls, conflicting reports, stalled financing.

- Outsourcing fits growing SMEs that need senior expertise without a full in-house team.

- NCSGX Canada delivers scalable support, compliance accuracy, reporting visibility, and cost efficiency.

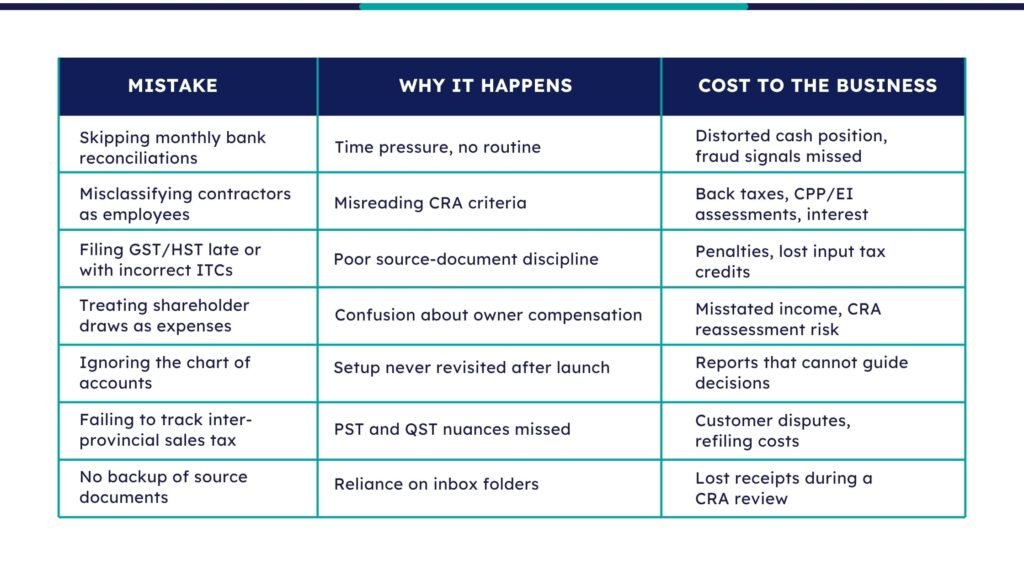

What Are the Most Common Bookkeeping Mistakes?

Reviewing hundreds of SME files reveals the same patterns. The mistakes are unglamorous, which is precisely why they go unnoticed.

These common bookkeeping mistakes do not sink into a company overnight. They compound. By year three, the cleanup cost often exceeds what it would have taken to set the function up properly from the start.

How Does Bookkeeping Improve Financial Resilience?

Financial resilience in business means a company can absorb revenue shock, tax adjustment, customer loss, or a sudden cost spike without losing operational control. The books are the foundation, because they decide how fast a leader sees what is happening and how confidently they can respond.

Resilient bookkeeping does five things at once:

- Surfaces cash flow risks before they become covenant breaches

- Produces lender-ready statements when financing windows open

- Keeps the business CRA-current and avoids penalty drag

- Feeds reliable management reports that support pricing and hiring decisions

- Shortens the time between a question and a defensible answer

CPA Canada has long emphasized that timely, accurate financial information is one of the strongest predictors of SME survival during economic turbulence. The Canadian companies that came through the 2020 to 2024 stretch intact were, almost without exception, the ones that already knew their numbers cold.

Warning Signs Your Books Need Attention

These signals suggest the bookkeeping function is no longer keeping pace with the business.

- You ask for a P&L and receive it more than five business days later

- Bank and credit card accounts go more than a month without reconciliation

- The same revenue line shows different totals across two reports

- Year-end always arrives with a long list of adjusting entries

- Sales tax filings rely on memory rather than recorded data

- The owner is still chasing invoices and entering bills personally

- Financing applications stall while books are “being cleaned up”

If three or more of these apply, the issue is structural, not personal. The fix is usually a better system and clearer ownership, not a harder-working bookkeeper.

Best Practices for Resilient Small Business Bookkeeping Services

The strongest finance functions inside Canadian SMEs tend to share a small set of habits.

Close the books monthly, not annually

A monthly close pulls problems forward when they are still small. It also produces twelve real data points each year, which makes forecasting credible.

Separate roles, even in small teams

Whoever approves payments should not be the same person who records and reconciles them. Segregation of duties is not just a control concept for large companies.

Use cloud bookkeeping with structured workflows

QuickBooks Online, Xero, and Sage are not differentiators. The discipline around them is. Source documents, naming conventions, and approval flows are what make the software earn its keep.

Build the chart of accounts around how you will read it

If management cannot read the P&L by service line, region, or product, the chart of accounts is not pulling its weight.

Document the cycle

A simple finance manual that names who does what, by when, in each month protects the business when someone is sick, leaves, or scales back.

Mini Case Study: A Toronto Professional Services Firm

A 22-person consulting firm in the GTA grew revenue from $3.1M to $4.6M over two years. Bookkeeping stayed where it began, with a part-time contractor reconciling quarterly. By the second year, the firm could not produce a clean trial balance for a credit line application. A 90-day cleanup recovered roughly $38,000 in missed input tax credits, corrected contractor classifications that had quietly exposed the firm to CRA for reassessment and reset the monthly close to a five business-day cadence. Financing went through on the second submission. The lesson was a familiar one: the books did not break the business, but they nearly cost it the next stage of growth.

Conclusion

Bookkeeping resilience is not really an accounting topic. It is a leadership topic dressed in accounting clothes. The Canadian SMEs that handle volatility well in 2026 will be the ones whose books stay current, whose filings run on routine, and whose reporting is fast enough to make decisions in real time. Strong small business bookkeeping services are how that becomes a system rather than a hope. NCSGX Canada partners with growing Canadian companies to build exactly that foundation.

How NCSGX Canada Can Help

NCSGX Canada works as a strategic bookkeeping and finance outsourcing partner for Canadian SMEs that have outgrown ad-hoc support but are not ready for a full in-house finance team. Engagements are built around four outcomes that founders, CFOs, and controllers care about.

Scalable support: Teams scale up during year-end, audits, financing rounds, or rapid growth, and scale back when the cycle eases. You pay for the capacity you actually need.

Compliance accuracy: GST/HST, PST, QST, payroll remittances, T4/T4A/T5 filings, and CRA correspondence are handled within a defined cycle, not on the back of someone’s calendar.

Reporting visibility: Monthly closes produce management reporting that leaders can read in five minutes and act on the same day. KPIs, cash flow forecasts, and variance commentary come standard.

Cost efficiency: Outsourced finance typically runs at a fraction of the loaded cost of comparable in-house seniority, with no recruitment lead time and no single-person risk.

If your books are slowing down your decisions, book a consultation with NCSGX Canada, or learn more about our bookkeeping and finance outsourcing services.

Frequently Asked Questions (FAQ)

1. What is the best bookkeeping software for businesses in Canada?

QuickBooks Online and Xero are the strongest all-rounders. Wave is excellent for very small businesses, and FreshBooks suits service-based work. The best fit depends on your industry, size, and growth plans.

2. Is cloud bookkeeping secure?

Yes, when you use reputable platforms. Leading providers offer bank-grade encryption, two-factor authentication, and automatic backups. In most cases, cloud security is stronger than what a typical small business could maintain on its own infrastructure.

3. Can bookkeeping software replace accountants?

No. Software handles data entry and reporting. Accountants and bookkeepers interpret the numbers, catch errors, manage CRA filings, and advise on decisions. The two work together.

4. Which bookkeeping app is best for startups?

Xero and QuickBooks Online both serve startups well. Xero tends to win for SaaS and tech-forward teams, while QuickBooks is strong for service businesses, retail, and trades.

5. How much does bookkeeping software cost in Canada?

Most plans range from free (Wave) to roughly $80/month CAD for advanced tiers. Most small businesses spend between $20 and $50/month CAD on software, plus the cost of a bookkeeper or outsourced provider.