USA

USA

Canada

Canada

Australia

Australia

The headlines have been relentless. Generative AI will replace half of your workforce. Hyperautomation will eliminate entire departments. Sustainability regulation will reshape every supply chain overnight. Read enough of this and you could be forgiven for thinking transformation is something that happens to organisations rather than something leaders drive with intention.

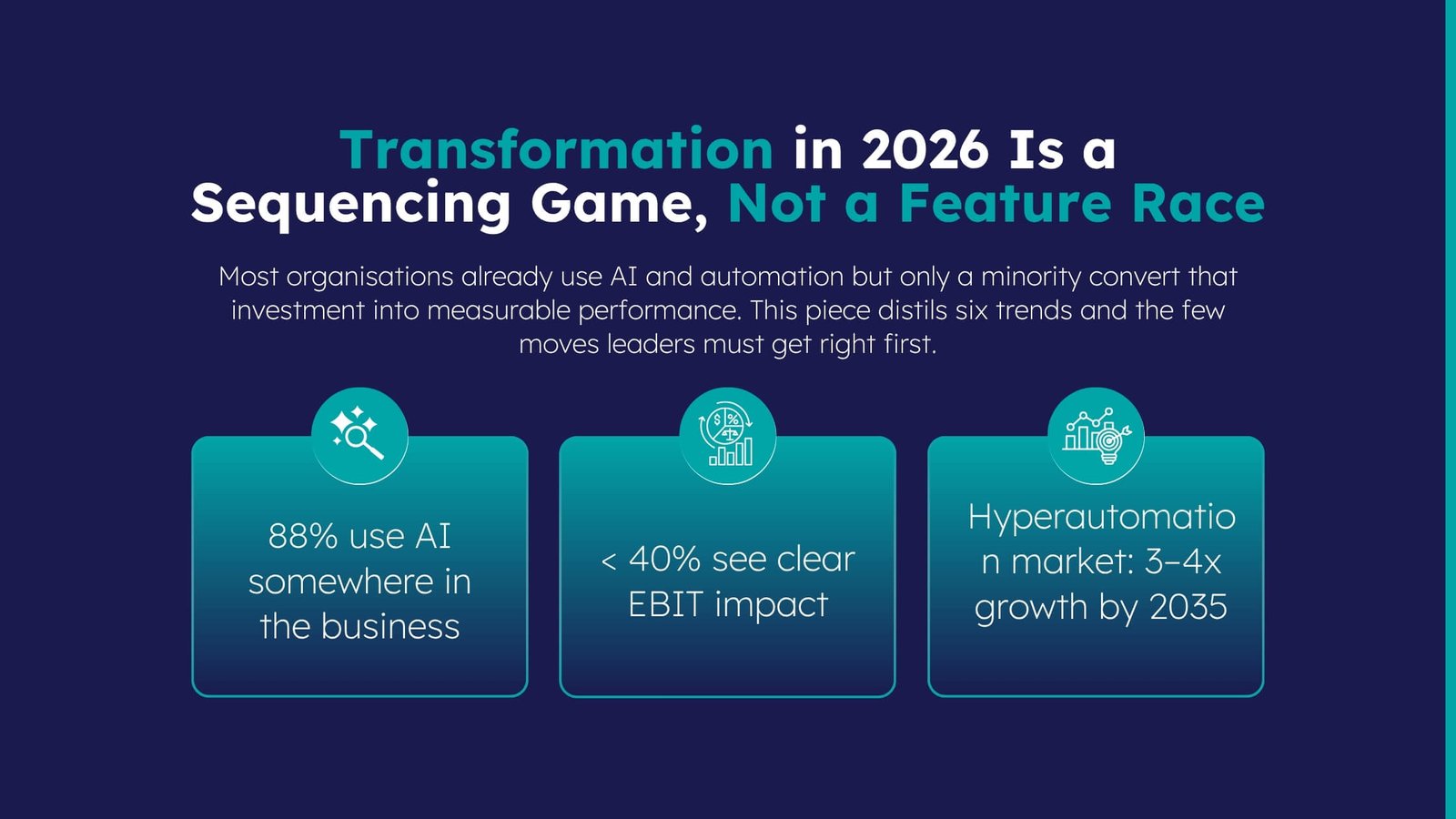

The reality inside most large enterprises is more measured and more interesting. Boards are balancing genuine urgency around AI and digital capability with the slower, harder work of operating model redesign, talent development, and risk governance. These business transformation trends for 2026 are not about novelty. They are about the moves that separate organisations convert investment into sustained performance from those that remain permanently in pilot mode.

Why 2026 Is a Pivot Year for Business Strategy

Three years ago, the dominant leadership posture toward AI was cautious about optimism: fund some experiments, track the business trends, wait to see what scaled. That posture has run its course. The organisations that spent 2023 and 2024 piloting are now facing a harder question why hasn’t it scaled?

McKinsey’s 2025 State of AI survey offers a useful frame: roughly 88% of organisations now use AI in at least one business function, yet only around a third have scaled it enterprise-wide, and fewer than 40% report clear EBIT impact. That gap between deployment and measurable value is the defining challenge of this moment, and it is a leadership and operating model problem, not a technology one.

Geopolitical fragmentation, tougher AI and ESG rules, and rising data‑privacy expectations are closing the window for inaction. At the same time, a widening AI skills gap means that by 2026, the risk of standing still is greater than the risk of moving thoughtfully.

Trend 1 – Generative AI 2026: From Pilots to Disciplined Value

The first phase of Generative AI 2026 adoption was about curiosity and access to deploy a tool, watch what employees do with it, and measure success by usage. The second phase demands something more rigorous: embedding AI into core workflows, integrating it into decision-support systems, and holding business units accountable for outcomes rather than activity.

- Gen AI usage has reached roughly 70–80% of organisations within just a couple of years, yet fewer than 40% report meaningful bottom‑line impact.

- The constraint is rarely the model; it is missing process redesign, unclear ownership, and governance that was never built to scale beyond early enthusiasts.

- Leading organisations now treat AI as an operating‑model question from the outset: which decisions to augment, which workflows to restructure, and which roles to redefine before choosing platforms or vendors.

- Deploying AI into a broken process simply makes that process faster and still broken; value comes from redesign plus disciplined measurement, not from tools alone.

What this means for leaders:

- Assign accountability for AI value realisation, separate from deployment at the business unit level.

- Identify the handful of workflows where AI changes unit economics, not just cycle time.

- Shift success metrics from tools deployed to redesigned processes with auditable, repeatable outcomes.

Trend 2 – Hyper Automation and End-to-End Intelligent Workflows

Hyper automation, sometimes written as hyperautomation, is the convergence of RPA, AI, process mining, low-code development, and orchestration tools to automate entire end-to-end processes, not isolated tasks. Most organisations that invested in RPA between 2018 and 2023 built “islands of automation”: fast, reliable bots handling one step while humans stitch everything together around them. Hyper automation replaces the stitching.

- The global hyperautomation market is expected to grow from about USD 76.9 billion in 2026 to over USD 300 billion by 2035, implying a CAGR in the mid‑teens, according to independent hyperautomation market research.

- Gartner and related industry analyses indicate that by 2026 roughly 30% of enterprises will automate more than half of their network activities, up from under 10% just a few years ago.

- This growth signals that hyperautomation is becoming a competitive necessity, not a discretionary experiment.

- Organisations that still treat automation as a point‑solution cost play are watching the gap to leaders widen faster than most boards recognise.

What this means for leaders:

- Audit your automation estate honestly: how much is genuinely end-to-end versus dependent on human handoffs between steps?

- Prioritise two or three high-volume, cross-functional processes, reconciliations, order-to-cash, onboarding, for full intelligent workflow redesign.

- Invest in process mining before buying more tools: you need visibility into actual processes, not documented ones.

Trend 3 – Proprietary Data, Ecosystems, and Context Engineering

The early AI arms race was about model capability. That race is largely over, foundation models are commoditising rapidly and are accessible to most organisations at broadly similar cost. The new competitive frontier is context: who can provide AI systems with the richest, most accurate, best-governed internal knowledge to function as genuine specialists rather than sophisticated generalists.

- Analysts and business schools tracking 2026 business trends increasingly highlight “context engineering” as a core discipline: structuring, governing, and surfacing proprietary knowledge, so AI operates with genuine domain expertise.

- A financial institution with a decade of clean, tagged client‑interaction data can extract far more value from the same model than a rival dependent on public data alone.

- This reframes data strategy as business strategy: proprietary data assets, integrated across systems and exposed via well‑designed APIs and ecosystem partnerships, are becoming the primary source of durable AI‑driven advantage.

What this means for leaders:

- Conduct a data asset audit: what proprietary knowledge, if properly governed, would make your AI systems genuinely differentiated?

- Build context engineering capabilities alongside AI deployment — not as a subsequent clean-up exercise.

- Treat APIs and ecosystem partnerships as strategic assets, not IT infrastructure decisions.

Trend 4 – Cyber Resilience and Digital Trust in an AI-First World

AI has changed the threat landscape in both directions. Attackers are using AI to automate reconnaissance, generate personalised phishing at scale, and identify vulnerabilities faster than most security teams can respond. Defenders are deploying AI-native platforms for faster detection and automated incident response. The net effect: the speed and cost of a serious security failure have both increased materially.

- Cybersecurity spending is projected to grow faster than overall IT budgets in 2026, signalling that boards are taking the risk landscape seriously.

- Yet many organisations still run cybersecurity and digital trust as parallel tracks to transformation—funded and governed separately, and engaged too late to shape programme design.

- McKinsey’s global AI trust research suggests only around 30% of organisations have reached mid‑level maturity or above in responsible‑AI governance and controls.

- Transformation programmes that proceed without a robust security and governance backbone are, in effect, building strategic platforms on ground that will not hold.

What this means for leaders:

- Integrate cyber resilience and responsible AI governance into transformation design from the outset, not as a workstream added after the architecture is set.

- Elevate CISO involvement to the transformation steering committee.

- Build explainability and auditability requirements into AI procurement as non-negotiable conditions, not optional features.

Trend 5 – Human-Centered, Skills-First Operating Models

The most consistent finding across underperforming AI programmes is not a technology failure. Skills were insufficient. Processes were not redesigned. Middle management lacked enough understanding to challenge AI-enabled decisions constructively. And change management was treated as a communications exercise rather than a structural intervention.

- HR and work‑futures research shows that while over 90% of HR leaders are involved in AI implementation, only about one in five have meaningful influence over AI strategy.

- That gap between involvement and strategic input is expensive: decisions on which roles AI should augment, where humans stay in the loop, and how employees build capability alongside AI are core strategy questions, not implementation details.

- Harvard Business Review–linked commentary on 2026 work trends warns about “workslop”: the accumulation of low‑quality AI output that quietly degrades decision‑making instead of improving it.

- Human‑centred, skills‑first operating models respond directly to these risks by pairing AI rollout with redesign of roles, capabilities, incentives, and challenge mechanisms.

What this means for leaders:

- Bring HR and people leadership into AI strategy decisions, not just deployment planning.

- Design human-in-the-loop checkpoints into high-stakes AI workflows as governance mechanisms, not friction to eliminate.

- Track “change fitness” as a formal KPI alongside cost and productivity metrics.

Trend 6 – Resilient and Sustainable Business Strategy

Sustainability has moved from aspiration to accountability. Net-zero commitments made in 2020 and 2021 are being measured against auditable baselines, Scope 3 reporting requirements, and institutional investors who want evidence of performance, not pledges. Simultaneously, geopolitical fragmentation, supply-chain rewiring, trade policy volatility, and energy cost unpredictability are driving an equally urgent conversation about operational resilience. Many boards are managing these as two separate workstreams. They are increasingly the same problem.

- Leading organisations are using digital transformation to redesign operating models that are more modular, less exposed to single points of failure, and aligned with carbon, due‑diligence, and reporting requirements.

- A manufacturer rethinking its supplier ecosystem to reduce Scope 3 emissions can simultaneously reduce supply‑chain concentration risk it was already worried about for other reasons.

- Treating resilience and sustainability as one integrated design problem avoids duplicated budgets and leadership attention that come from running them as separate tracks.

- Quiet, structural embedding of sustainability and resilience into core operations consistently outperforms loud, performative efforts in both credibility and long‑term value creation.

What this means for leaders:

- Consolidate resilience and sustainability planning within transformation governance rather than running parallel programmes.

- Design for modularity: operating models flexible by region, product line, or supply pathway are both more resilient and more sustainable.

- Anticipate tightening regulation across carbon reporting, supply-chain due diligence, and AI governance simultaneously and plan, rather than react.

Where Leaders Should Focus in the Next 12–18 Months

Six trends are a lot to absorb, and programmes that chase all of them at once usually move none of them meaningfully forward. The discipline in 2026 is to pick a small number of critical moves and execute them with real rigour, not spread effort thinly across every new idea. And across all six trends, the real distance between investment and value is set far more by operating models, governance, and people’s decisions than by technology itself.

Four priorities stand out for the next 12 to 18 months:

- Start with AI in your own decision-making: Leadership teams that have not engaged personally with AI tools lack the judgment to govern deployment at scale. Experimentation at the top accelerates credibility throughout the organisation.

- Pick one or two end-to-end processes for full hyper automation: Avoid spreading automation investment thinly. Go deep on a small number of cross-functional flows, measure rigorously, and use those results to build the case for broader roll-out.

- Treat data, security, and governance as strategic investments: Budget decisions that separate these from transformation programmes create structural risk and dilute the value of everything else.

- Elevate HR into transformation strategy: Skills, culture, and change management are frequently the primary determinant of whether transformation is delivered. Organisations that recognise this early will close the pilot-to-performance gap faster than those that add it as an afterthought.

Conclusion

In 2026, transformation is less about chasing every shiny new capability and more about choosing a small number of pivotal moves, sequencing them wisely, and out‑executing the competition. Leaders who apply that level of discipline will not just ride disruption; they will define the operating model benchmarks that others spend the next decade trying and failing to replicate. If you are ready to move from pilots to performance, start a conversation with NCSGX about how to sequence and deliver those moves in your organisation.

How NCSGX Can Help?

Knowing the trends is one thing, translating them into disciplined, measurable action is another. At NCSGX, we work with leadership teams to move beyond the pilot phase and build the operating model foundations that turn AI, automation, and digital investment into sustained performance. From redesigning end-to-end workflows to aligning people’s strategy with transformation goals, we bring the strategic depth and execution capability to close the gap between ambition and outcome. If you are ready to stop cycling through pilots and start delivering results, speak with NCSGX today.