USA

USA

Canada

Canada

Australia

Australia

Introduction

It’s common for businesses to pay for services before using them, earn revenue before sending an invoice, or receive customer payments before completing the work. While these situations happen every day, recording them correctly is what keeps financial statements accurate.

At NCSGX, we help businesses maintain accurate financial records by applying accrual accounting principles consistently throughout the bookkeeping process. From recording prepaids, accruals and deferrals to managing month-end adjustments, our bookkeeping professionals help ensure financial statements reflect the true financial performance of the business, enabling more informed decision-making.

Accrual bookkeeping workflows: prepaids, accruals and deferrals explained

Accurate financial reporting is not just about recording money as it moves in and out of your bank account. It’s about matching revenue with the expenses incurred to earn it during the same accounting period. This principle helps businesses understand their actual financial performance instead of simply tracking cash flow.

That’s where Prepaids, Accruals, and Deferrals come into play. These adjustments are essential components of accrual basis accounting, ensuring financial statements reflect economic activity rather than payment dates.

Whether you’re a Canadian small business owner, startup founder, or finance manager, understanding these concepts can make month-end bookkeeping more accurate and less stressful. In this guide, we’ll explain how prepaids, accruals, and deferrals work, when to record them, and why they matter for reliable financial reporting.

Accrual vs cash basis:

The main difference between cash and accrual accounting is the timing.

Under cash accounting, revenue and expenses are recorded only when cash changes hands. While this approach is straightforward, it may not always reflect your business’s actual financial position.

Under an accrual basis of accounting, transactions are recorded when they are earned or incurred, regardless of when payment is received or made. This provides a more complete picture of business performance during each reporting period.

Many Canadian businesses use accrual accounting because it aligns with generally accepted accounting principles and provides more meaningful financial information for decision-making. For businesses looking to better understand financial reporting principles, CPA Canada provides guidance on accounting concepts and financial reporting standards.

Key Takeaways

- Prepaid expenses are payments made in advance and are initially recorded as assets before being recognized as expenses over time.

- Accruals ensure revenue and expenses are recorded when they are earned or incurred, even if cash hasn’t yet changed hands.

- Deferred revenue represents customer payments received in advance and is recognized as revenue only as goods or services are delivered.

- Adjusting journal entries help keep financial statements accurate by recording prepaids, accruals, and deferrals at month-end.

- Following a consistent month-end bookkeeping workflow improves reporting accuracy and supports better financial decision-making.

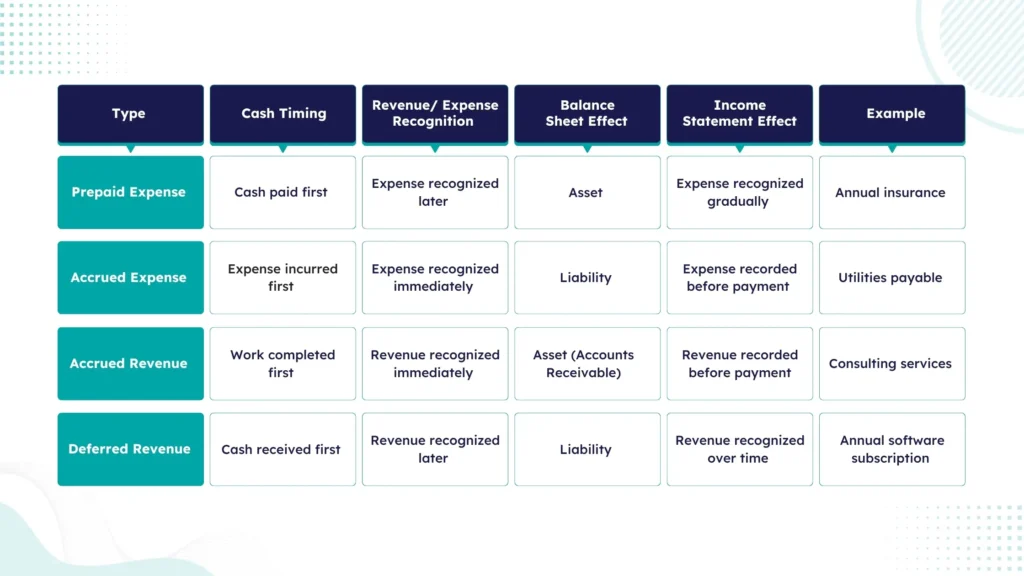

Prepaids: paying now for something you’ll use later

A prepaid expense is a payment made before receiving the full benefit of a product or service.

Instead of recording the entire payment as an expense immediately, it is first recorded as an asset because it represents future economic value. As the business uses that benefit over time, the prepaid amount is gradually recognized as an expense.

Common Canadian examples include:

- Annual business insurance premiums

- Annual software subscriptions

- Office rent paid several months in advance

- Equipment maintenance contracts

Why prepaid expenses are assets initially

Imagine your company pays $12,000 on January 1 for one year of commercial insurance.

Although the cash has left your account, you haven’t consumed the entire year’s insurance coverage on the first day. At that point, your business still has the right to receive insurance protection over the next twelve months.

Therefore, the payment is initially recorded as a prepaid asset.

Initial journal entry

| Account | Debit | Credit |

| Prepaid Insurance | $12,000 | |

| Cash | $12,000 |

At the end of each month

| Account | Debit | Credit |

| Insurance Expense | $1,000 | |

| Prepaid Insurance | $1,000 |

Simple timeline

January 1

Pay $12,000 insurance → Recorded as a prepaid asset.

End of January

Recognize $1,000 as insurance expense.

End of December

The prepaid asset balance reaches zero, and the full expense has been recognized.

This approach follows the matching principle by spreading the expense across the period that benefits from insurance coverage. Maintaining these adjustments throughout the year can also reduce reconciliation issues and help avoid extensive Bookkeeping Cleanup before financial reports are prepared.

Accruals: recording before the invoice or payment

Accruals recognize revenue or expenses that have been earned or incurred but have not yet been billed, paid, or received.

Without accruals, financial statements may understate expenses or revenue, making profitability appear higher or lower than it actually is.

There are two common types of accruals.

Accrued expenses

An accrued expense is a cost your business has already incurred but has not yet paid.

Examples include:

- Employee wages earned before payday

- Utility bills received after month-end

- Legal or accounting services already performed

- Interest accumulated on loans

Example

Suppose your electricity provider sends the invoice on April 5 for electricity used during March.

Even though payment hasn’t been made, March should include the expense.

Month-end adjusting journal entry

Account | Debit | Credit |

Utilities Expense | $850 |

|

Accrued Liabilities |

| $850 |

When the invoice arrives

Account | Debit | Credit |

Accrued Liabilities | $850 |

|

Cash |

| $850 |

This prevents expenses from being recorded twice.

Accrued revenue

Accrued revenue represents income your business has earned but has not yet invoiced or collected.

This situation commonly occurs when services are completed near the end of the month.

Example

A consulting firm finishes a project worth $7,500 on June 29 but issues the invoice on July 3.

Revenue belongs in June because the work was completed during that month.

Adjusting journal entry

Account | Debit | Credit |

Accounts Receivable | $7,500 |

|

Service Revenue |

| $7,500 |

Journal entry when payment is received

Account | Debit | Credit |

Cash | $7,500 |

|

Accounts Receivable |

| $7,500 |

This ensures that June’s income statement reflects the revenue earned during June.

Deferrals: getting paid now for work you haven’t done

Deferrals are essentially the opposite of accruals.

In this case, the business receives payment before earning the revenue.

Since the service or product has not yet been delivered, the money cannot immediately be recognized as revenue. Instead, it is recorded as a liability called deferred revenue or unearned revenue.

Common examples include:

- Annual software subscriptions

- Website maintenance contracts

- Consulting retainers

- Annual service agreements

Why deferred revenue is a liability

Suppose a software company receives $24,000 upfront for a one-year subscription.

The customer has paid, but the company still owes twelve months of service.

Therefore, the amount represents an obligation not earned income.

Initial journal entry

Account | Debit | Credit |

Cash | $24,000 |

|

Deferred Revenue |

| $24,000 |

Each month

Account | Debit | Credit |

Deferred Revenue | $2,000 |

|

Subscription Revenue |

| $2,000 |

Monthly timeline

January

Customer pays annual subscription.

February–December

One month’s revenue is recognized each month.

End of contract

Deferred revenue balance reaches zero because all services have been delivered.

Recognizing revenue gradually ensures financial statements accurately reflect the services provided during each reporting period. This treatment is consistent with the recognition principles outlined in the IFRS Conceptual Framework, which supports presenting financial information that faithfully represents a business’s financial performance.

Prepaids vs accruals vs deferrals

Where these fit in a month-end bookkeeping workflow

Month-end bookkeeping involves more than reconciling bank accounts. Adjustments ensure financial statements accurately reflect business activity during the reporting period.Step 1: Review prepaid expenses

Identify payments made in advance and recognize the portion that applies to the current month. ⮟Step 2: Identify accrued expenses

Record expenses incurred but not yet invoiced, such as wages, utilities, interest, or professional fees. ⮟Step 3: Record accrued revenue

Recognize revenue for work completed before month-end, even if the invoice has not yet been issued. ⮟Step 4: Adjust deferred revenue

Move the earned portion of customer prepayments from deferred revenue to revenue. ⮟Step 5: Post adjusting journal entries

Record all necessary adjustments to ensure revenues, expenses, assets, and liabilities are accurate. ⮟Step 6: Review financial statements

Check the income statement and balance sheet to confirm all month-end adjustments have been reflected correctly. Following this workflow each month improves consistency, supports better decision-making, and reduces the risk of reporting errors.Common mistakes to avoid

Even businesses that maintain accurate day-to-day bookkeeping can overlook month-end adjustments. Some of the most common mistakes include:

Expensing prepaid items immediately

Recording an entire annual insurance premium or software subscription as an expense in one month can distort profitability.

Forgetting accrued expenses

Missing payroll, utility, or interest accruals can understate liabilities and overstate net income.

Treating deferred revenue as immediate income

Recognizing customer payments before delivering goods or services can overstate revenue and create misleading financial statements.

Missing adjusting journal entries

Without adjusting entries, financial statements often fail to reflect the true timing of revenues and expenses.

Skipping month-end reviews

Regular month-end reviews help identify missing accruals, prepaid adjustments, and deferred revenue balances before financial reports are finalized. Pairing regular reviews with virtual bookkeeping can make it easier to identify issues throughout the month instead of waiting until month-end.

Conclusion

Accrual accounting provides a more accurate view of your business’s financial performance by recognizing revenue and expenses when they are earned or incurred not simply when cash changes hands. Understanding prepaids, accruals and deferrals helps improve the accuracy of financial statements, strengthens your month – end bookkeeping workflow, and supports more informed business decisions. Businesses should also ensure their accounting practices are consistent with applicable Canada Revenue Agency (CRA) reporting requirements where relevant.

As your business grows, managing adjusting journal entries, accruals, and month-end reconciliations can become increasingly complex. At NCSGX, we help Canadian businesses streamline their bookkeeping processes with accurate, reliable accounting support tailored to their needs. If you’re looking to improve the accuracy of your financial reporting or simplify your month-end close, contact our team to learn how we can help.

How NCSGX Can Help

Applying prepaids, accruals, deferrals, and other adjusting journal entries correctly requires consistency and attention to detail, especially as your business grows. At NCSGX, we help Canadian businesses maintain accurate accrual-based bookkeeping through reliable month-end processes, timely adjusting entries, account reconciliations, and financial reporting. Our team works to ensure your financial records accurately reflect your business activity, giving you greater confidence in every reporting period.

Whether you need ongoing bookkeeping support or assistance improving your month-end close, our experienced professionals can help simplify your accounting processes while reducing the risk of reporting errors. With accurate, up-to-date financial records, you can make informed business decisions, stay prepared for tax reporting, and focus on growing your business instead of managing complex bookkeeping adjustments.

Frequently Asked Questions (FAQ)

1. Is deferred revenue the same as prepaid?

No. They are opposite sides of a transaction. Deferred revenue is money received from a customer before delivering goods or services (a liability), while a prepaid expense is money your business pays in advance for future benefits (an asset).

2. Do I need accrual accounting for the CRA?

It depends on your business and the type of income you report. Many Canadian businesses use accrual accounting because it provides a more accurate picture of income, but CRA requirements can vary. When in doubt, consult a CPA or tax professional.

3. What's a reversing entry and do I need one?

A reversing entry is an optional journal entry made at the start of a new accounting period to reverse certain adjusting entries from the previous period. It isn’t mandatory but can simplify bookkeeping and help prevent duplicate entries.

4. What are prepaids, accruals and deferrals in accrual bookkeeping?

Prepaids, accruals, and deferrals are accounting adjustments that ensure income and expenses are recorded in the correct reporting period. They help financial statements reflect business activity rather than simply when cash is received or paid.

5. What is the difference between prepaid vs accrued expense?

A prepaid expense is paid before the benefit is received and is initially recorded as an asset. An accrued expense is incurred before payment is made and is recorded as a liability until it is paid.

6. Do Canadian businesses need accrual accounting for CRA reporting?

Many Canadian businesses prepare their financial records using the accrual method because it aligns income and expenses with the period they relate to. The appropriate method depends on your business and CRA requirements, so professional advice may be appropriate.